Navigating International VAT Schemes (OSS/IOSS)

Cross-border sales within the EU used to mean a separate VAT registration in every destination state once thresholds were breached. The 2021 e-commerce package rewrote the rulebook.

-

Union One-Stop-Shop (OSS) for EU-based sellers of goods and digital services to consumers.

-

Non-Union OSS for non-EU sellers of digital services.

-

Import One-Stop-Shop (IOSS) for consignments valued below €150 shipped from outside the EU.

For a detailed guide on when and how to use the OSS/IOSS, don't miss VAT in European Union: EU VAT Rules Explained for International Sellers.

These schemes collected over €33 billion in VAT during 2024, with €24 billion declared under Union OSS alone. Registrations keep rising, passing 170,000 businesses by the end of 2024.

When OSS/IOSS Beats Multiple Registrations

-

Your goods ship from one EU warehouse to shoppers in several member states.

-

Digital services flow automatically online with customer downloads.

-

Low-value parcels (< €150) dispatch daily to EU buyers from outside Europe.

Instead of juggling returns in France, Spain, and Italy, you file one OSS return in your chosen “Member State of Identification”. That saves translation costs and headaches.

Looking for practical compliance and common pitfalls? See the VAT Compliance for SaaS and Digital Services in the EU for best-practice guidance on threshold management and compliant invoicing.

Still, OSS does not solve every scenario. Holding inventory in multiple EU countries, or B2B sales, could trigger local registrations. Specialist teams like 1stopVAT evaluate warehouse footprint, supply chain, and transaction mix to decide whether a hybrid model makes sense.

Stay Compliant or Deregister When Eligible

Getting the number is half the story. Keeping it - or letting it go-matters just as much.

Ongoing Compliance Checklist

-

File returns on schedule: late filings may attract surcharges as high as 15% in some EU states.

-

Pay VAT due in full: partial payments accrue daily interest.

-

Keep digital records for the statutory retention period (often 10 years).

-

Reconcile sales platforms and bank statements quarterly to catch errors early.

For a deeper dive into compliance triggers, threshold monitoring, and the importance of document retention, see the VAT Deregistration: When and How to Deregister Your Business.

When and How to Deregister

Your business can deregister if turnover falls below a national deregistration threshold. In the UK, voluntary deregistration is possible when taxable turnover drops below £88,000. Roughly 218,000 UK traders did so in 2024–25, a reminder that deregistration is common.

Steps to deregister:

-

Submit an online request and final return.

-

Pay any outstanding VAT or reclaim balance owed.

-

Remove VAT from invoices after the official cancellation date.

Ceasing to trade? Retain records for the mandated years because audits may still occur.

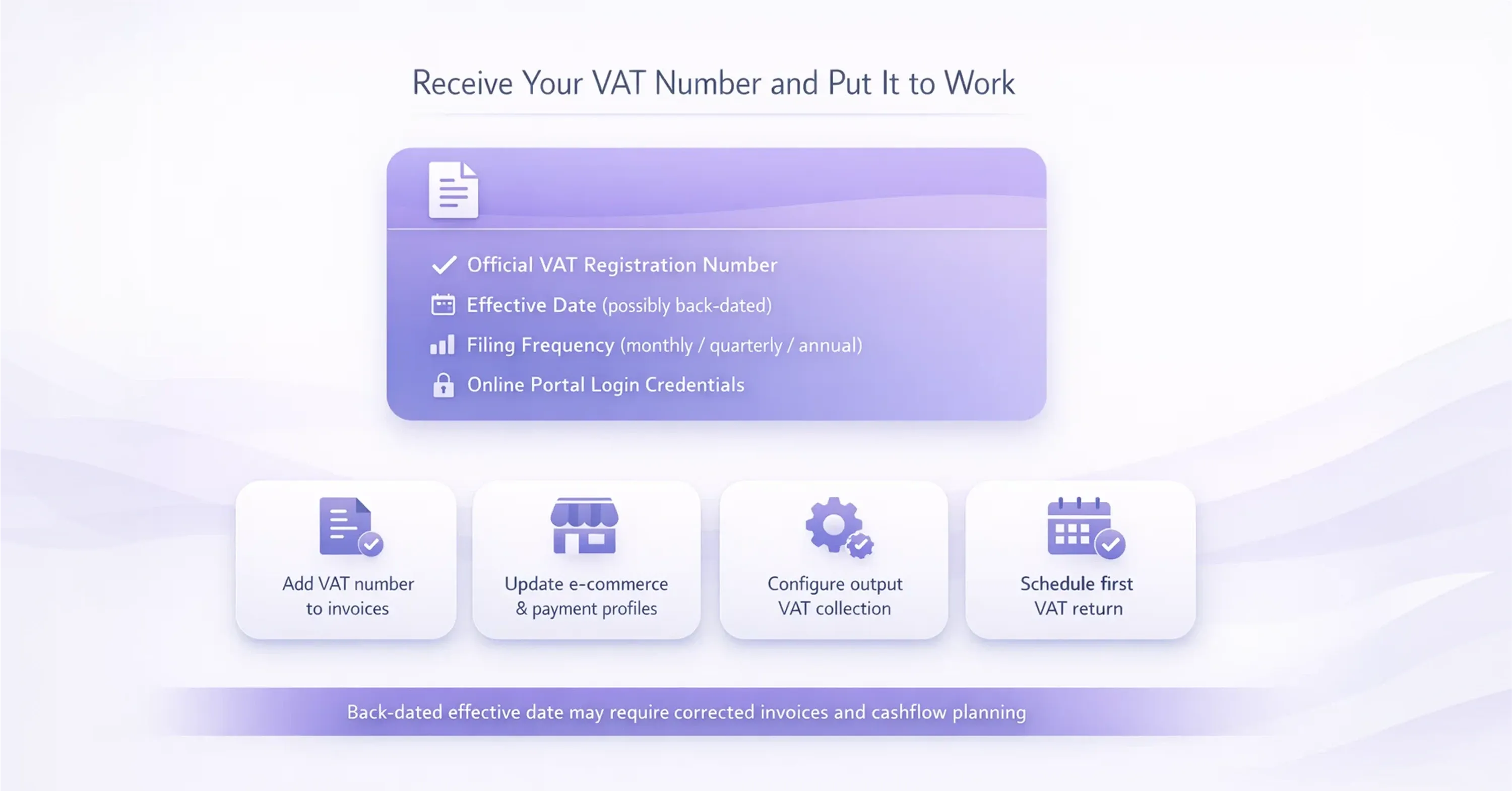

5-Point VAT Registration Checklist

Need a lightning summary? To register for VAT you must: 1) Verify your turnover exceeds the national threshold, 2) Collect ID, bank, and address documents, 3) Choose the correct registration route (domestic, non-resident, or OSS/IOSS), 4) Complete the online VAT application accurately and submit scans, 5) Add the issued VAT number to invoices and file returns from the effective date.

Conclusion

Vat tax registration is less about filling forms and more about understanding where your business fits in the VAT ecosystem. First, confirm you need to register, then gather airtight documentation, pick the right route, and submit a precise application. After your VAT number arrives, invoice correctly, file on time, and monitor turnover for potential deregistration. When global expansion beckons, schemes like OSS/IOSS and advisory partners such as 1stopVAT can simplify multinational compliance while you focus on growth.