What you will learn

By the end, you will know exactly which member state you must register in, which online portals to use, and how to avoid the errors that cause most applications to be rejected. Along the way we cite real numbers- such as the €33 billion declared through the EU’s OSS schemes in 2024 - and show how the system is getting faster and more digital each year.

Below is a concise checklist you can bookmark. After that we explore each step in detail and flag the common traps.

EU VAT registration at a glance

EU VAT registration involves seven core actions:

-

Confirm your obligation (thresholds, distance-selling, or non-resident rules).

-

Select your Member State of identification (MSI).

-

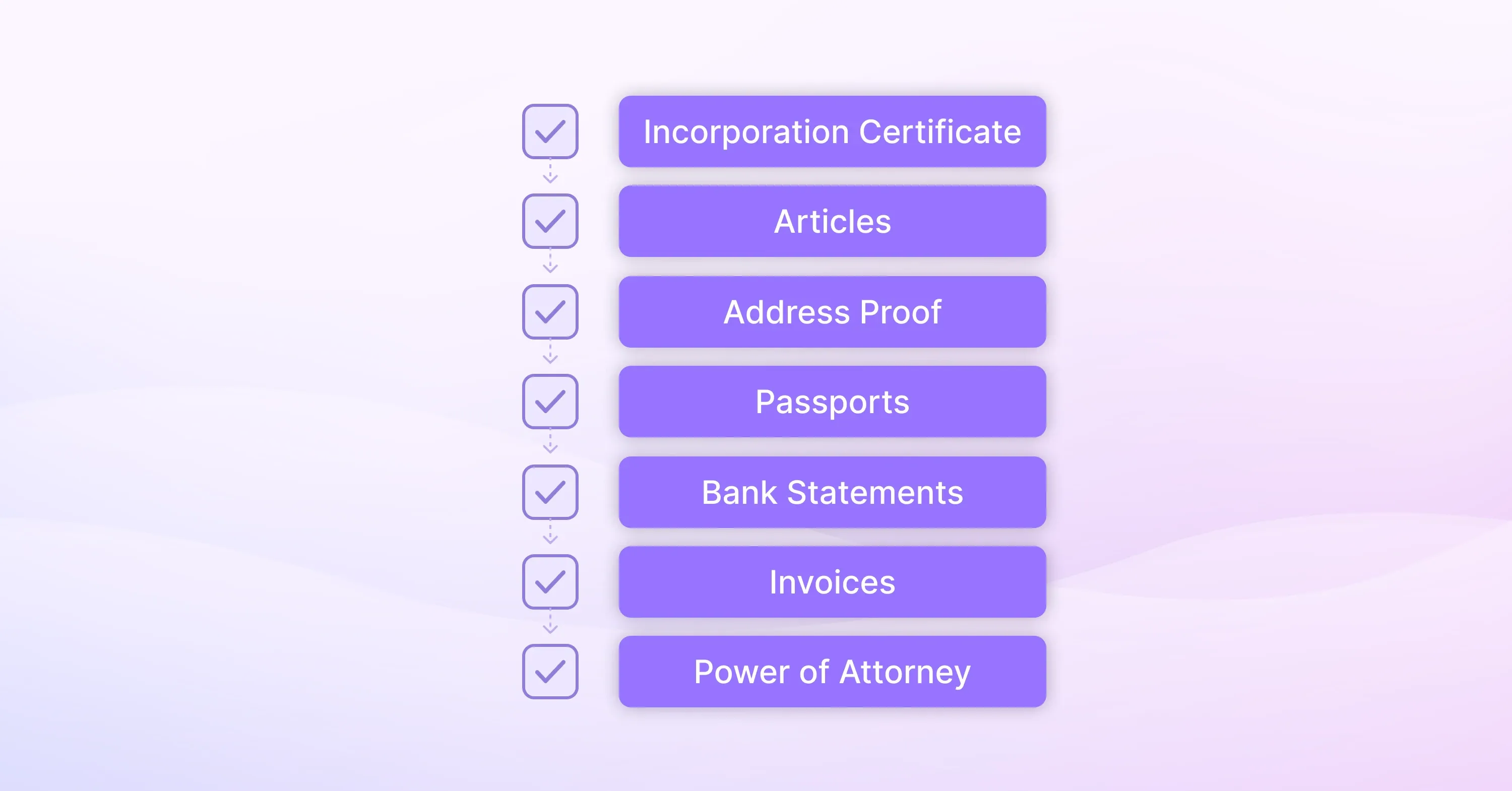

Gather legal, banking, and trade documents.

-

Create an account in the national tax portal.

-

Submit the application form and copies of documents.

-

Receive and verify your VAT number.

-

Set up filings, OSS/IOSS where eligible, and keep records for 10 years.

Step 1: Confirm whether you must register

Even before filling out a form, you need absolute clarity on when EU VAT registration is mandatory. The rules vary slightly across member states but share three triggers.

-

Selling goods within a country where you hold stock or have a permanent establishment: immediate registration.

-

Cross-border B2C sales of goods that push the €10,000 EU-wide distance-selling threshold: register either in each destination country or opt for the Union OSS.

-

Providing digital services to EU consumers when you exceed the same €10,000 threshold: register or use the non-Union OSS.

Businesses ignore these limits at their peril. VAT fraud already costs governments tens of billions of euros each year, with compliance pitfalls detailed in the VAT Compliance: How EU Businesses Lost €159M in Penalties article. That pressure fuels stricter audits, so the margin for error is shrinking.

A UK cosmetics brand stored inventory in Poland to speed deliveries. Because stock physically sat in Poland, it had to register for Polish VAT before the first sale, even though projected turnover was only €3.000 per month.

Failing the obligation check is the root cause of many fines. Once you are sure you need a number, you can decide where to file.

The next section bridges from the “if” to the “where”.

Step 2: Choose the right Member State of identification

Your Member State of identification (MSI) determines the portal you use, the language of correspondence, and sometimes the speed of approval. Broadly, you have three scenarios.

-

Established in an EU country: register in your home state for domestic VAT and optionally add Union OSS for cross-border B2C sales.

-

Non-EU seller without EU stock: pick one EU country as your MSI under the non-Union OSS for digital services.

-

Non-EU seller with stock inside the EU: register in each country where goods are stored and, if using warehouses in several countries, consider multiple local numbers plus Union OSS for distance sales.

Why does the choice matter? Because refusal rates differ. Romania, for instance, cut its share of rejected applications from 14.5% in 2016 to just 2.2% in 2019 as highlighted in an EU report on VAT control procedures. Choosing a jurisdiction with clear guidance and user-friendly portals saves weeks. Practical decisions on country and scheme combinations are explored in the Fast-Track VAT Registration: How to Register Quickly and Easily guide.

Conclude the decision by noting each country’s language, required sworn translations, and whether you need a fiscal representative (mandatory in, say, Italy for most non-EU traders). Now you can start the document hunt.