Overview

Making Tax Digital VAT is now a mandatory requirement for all VAT-registered businesses in the UK, yet many companies still struggle to understand what full compliance actually involves in practice. From digital recordkeeping to software-based submissions, the shift to MTD has fundamentally changed how VAT is managed and reported.

This guide explains everything businesses need to know about Making Tax Digital for VAT, including who must comply, key deadlines, and how to set up MTD-compatible systems. It also breaks down the practical steps to automate VAT filing and maintain accurate digital records over time. Whether you're transitioning from spreadsheets or optimizing an existing setup, this article provides a clear path to achieving and maintaining VAT digital compliance.

What Making Tax Digital VAT Actually Requires

Making Tax Digital (MTD) for VAT is HMRC's programme to move VAT administration from paper and spreadsheets into compatible digital software.

The core obligation has two parts:

-

Digital recordkeeping: You must store VAT records (sales, purchases, VAT account summaries) in a digital format using functional compatible software, not in paper ledgers or standalone spreadsheets.

-

Digital submission: Your VAT return must be filed directly from that software to HMRC via an Application Programming Interface (API). Manual re-keying of figures into HMRC's online portal no longer satisfies the rules.

Think of it this way: if your bookkeeper previously typed totals from a spreadsheet into the HMRC website, that process is no longer compliant. The software itself must transmit the nine-box return data.

The programme isn't unique to the UK. Governments worldwide are digitising tax reporting. The OECD confirms that digital reporting and effective audits have played a significant role in reducing the VAT gap in recent years. The EU, for instance, saw its VAT compliance gap fall from roughly €121 billion in 2018 to about €89 billion in 2022. Digital mandates are the clear direction of travel.

Who Must Comply with HMRC VAT Rules for MTD

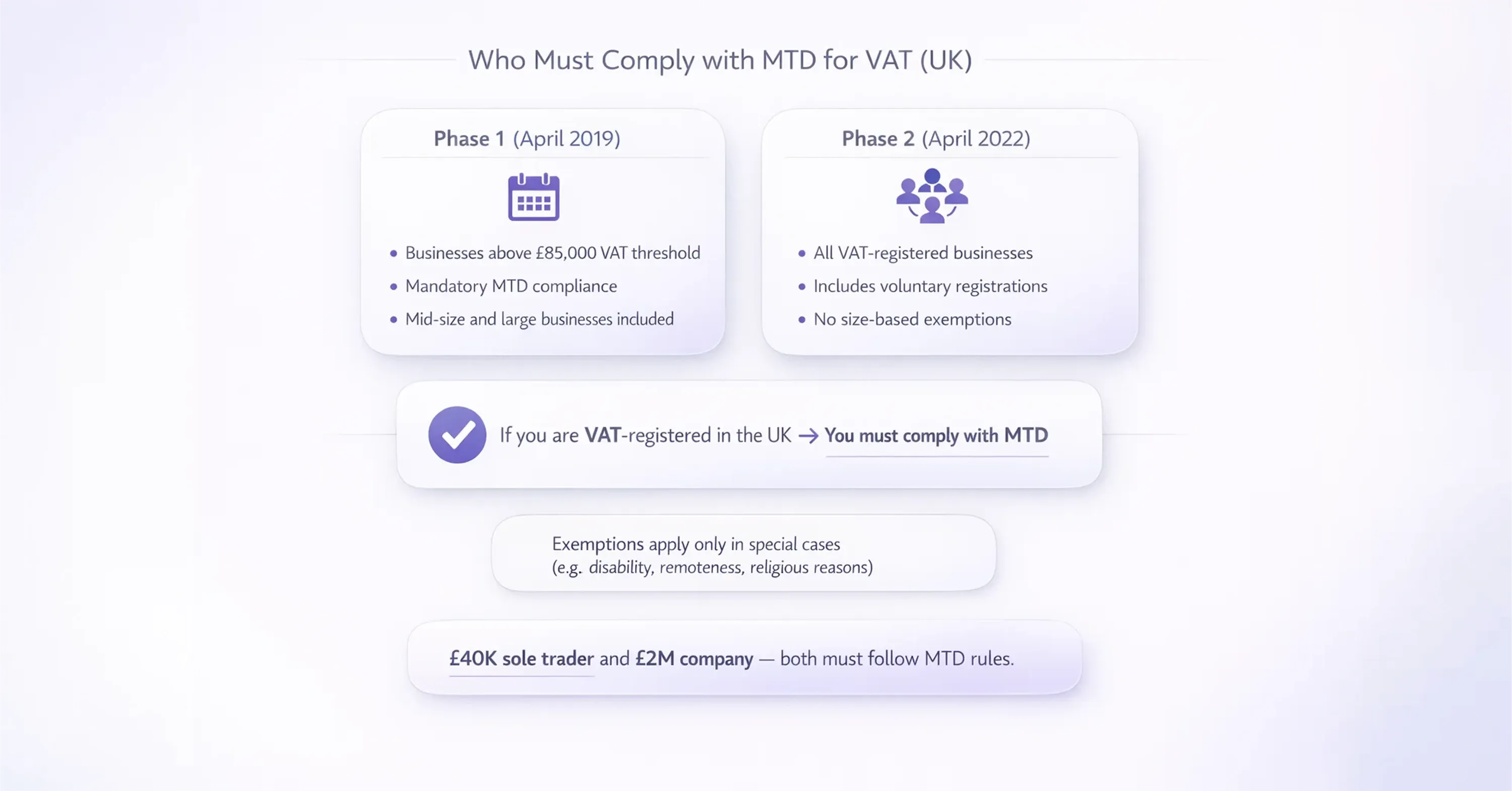

MTD for VAT rolled out in two phases, and both are now fully in effect.

Phase 1: Above the VAT Threshold (April 2019)

Businesses with taxable turnover above £85,000 were required to join MTD from their first VAT period starting on or after 1 April 2019. This covered the majority of mid-size and larger VAT-registered businesses.

Phase 2: Below the VAT Threshold (April 2022)

From April 2022, all remaining VAT-registered businesses, including those voluntarily registered with turnover below £85,000, were brought into scope. There are no longer any VAT-registered businesses exempt from MTD simply because of their size.

In practical terms, if you have an active UK VAT registration, you must comply. The only businesses outside MTD for VAT are those that have received a specific exemption from HMRC, typically on grounds such as disability, age, remoteness of location, or religious objections to using electronic communications.

For example, a sole trader selling handmade goods online who voluntarily registered for VAT at £40,000 turnover is just as bound by MTD as a £2 million-revenue wholesaler. Both need compatible software and digital submissions.

For more on eligibility and practical registration steps, see the guidance in How to Register for VAT: A Complete Guide.

Now that you know who's in scope, let's look at the deadlines and filing rhythm you need to follow.