Why Deadlines Slip: Common Pitfalls

Even organised finance teams miss deadlines. Understanding the behavioural and structural triggers helps you design countermeasures.

-

Fragmented data sources: sales platforms, payment gateways, and ERP systems do not reconcile automatically.

-

Staff turnover: new hires often inherit incomplete process notes.

-

Cash-flow prioritisation: delaying payment to preserve liquidity leads to missed submissions.

-

Manual filing fatigue: despite widespread e-filing, about 57 million tax returns were still on paper as of 2022, showing manual processes persist.

Leaving these issues unresolved feeds late filings, so the next part offers practical ways to stay ahead.

Staying Compliant: Practical Tips and Tools

Adopting proven habits and the right support structures keeps your VAT filing schedule intact.

-

Move to e-filing: 95% of business tax returns in OECD countries are already electronic, confirming that digital is mainstream and reliable.

-

Calendar reminders with owner accountability: assign names beside each task in the schedule, not just dates.

-

Reconcile weekly, not quarterly: smaller data sets are easier to check and fix.

-

Contingency workflow: have a two-person review if the main preparer is absent.

-

Specialist support: a VAT compliance partner like 1stopVAT, whose team of 40+ certified specialists covers more than 100 jurisdictions, can centralise registrations and filings so businesses meet every deadline while expanding abroad.

For an actionable compliance framework, explore VAT Filing & Returns: A Complete Guide for Businesses.

By embedding these habits, you make compliance a natural by-product of daily operations, not a stressful month-end project. The emphasis on preventative structure concludes the narrative arc, leaving only the most common quick-reference queries.

Conclusion

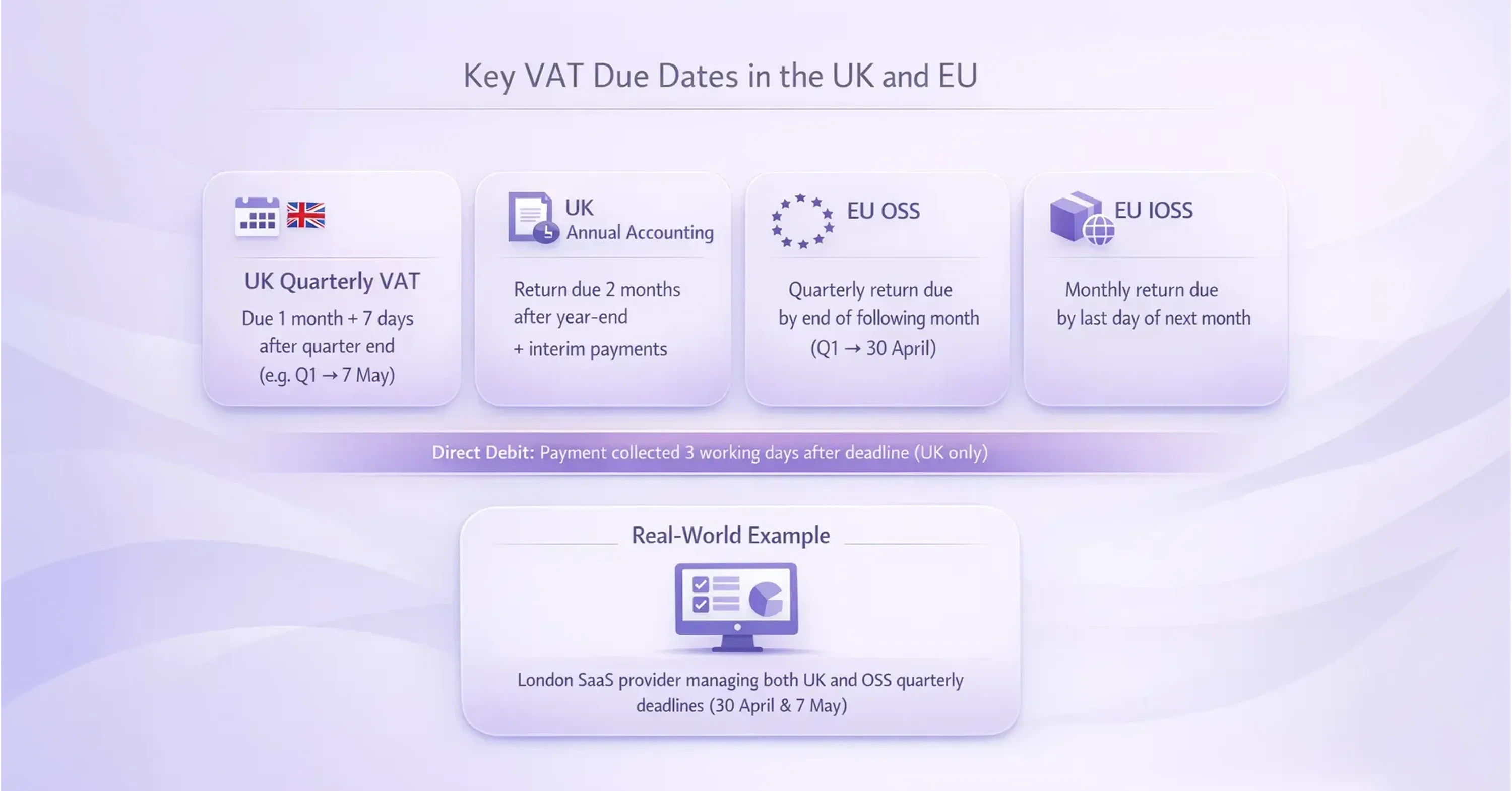

VAT compliance is a recurring race against the clock. From the UK’s “one month plus seven days” rule to EU OSS month-end submissions, the calendar is unforgiving. Penalties add up fast, with each late filing bringing you closer to a £200 charge and potential interest.

The good news is that disciplined processes, electronic filing, and, where needed, expert support can keep every deadline within reach. By mapping your VAT due dates, monitoring your points balance, and maintaining clear internal ownership, you transform filing from an annual headache into a routine task that protects cash flow and reputation alike.

If you’re wondering when to file or how to prepare each monthly or quarterly return, this VAT Return: When to File and How to Prepare checklist breaks the process down step-by-step.

For best practices on recordkeeping, digital workflow, and automation, see VAT Reporting Made Simple: Best Practices for Businesses.

If your business files in multiple countries or is scaling its cross-border operations, practical support is available. Discover how dedicated experts can ensure compliance in every jurisdiction: VAT Compliance & Consultancy: Why Expert Advice Matters.