The Core Steps for VAT Returns

To file a VAT return, a business calculates the total VAT on sales and purchases for the reporting period, then submits this figure - along with the corresponding payment or refund request - to HMRC before the stated deadline. Consistent record-keeping is crucial for accuracy and compliance.

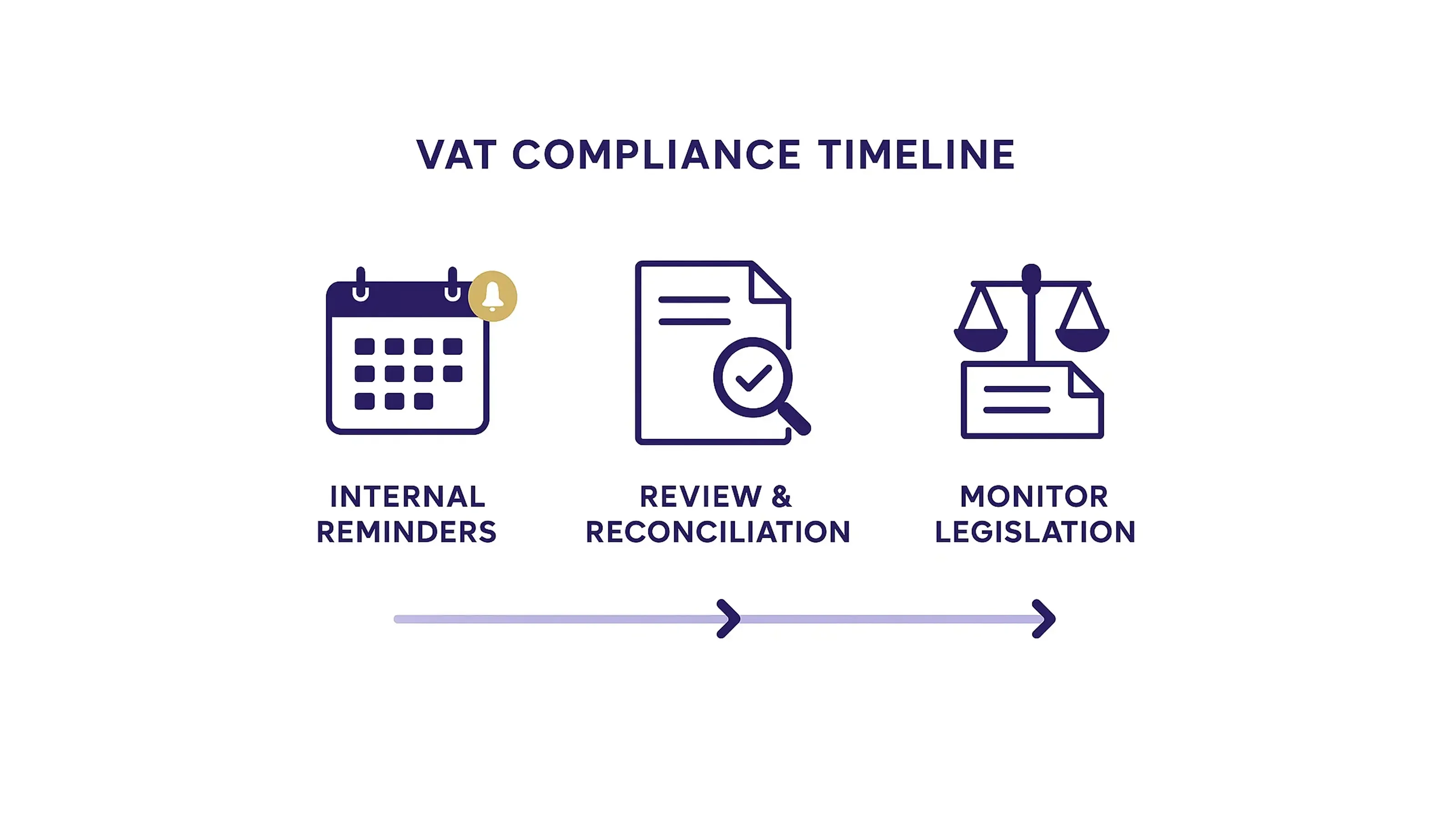

Step 6: Track Ongoing Compliance

Filing doesn’t end once you hit “submit.” Staying on top of your obligations requires a clear system:

Internal Reminders

- Automate your calendar so you never miss monthly cutoffs.

- Set up email alerts for upcoming deadlines.

Review and Reconciliation

- Compare your actual transactional data to your submitted figures.

- Investigate any discrepancies right away, since unresolved errors might trigger issues later.

Monitor Shifting Legislation

- HMRC’s guidelines on tax thresholds and reporting sometimes change.

- Pay attention to public releases, such as the HMRC Annual VAT Statistics 2023–24, which note £168 billion in VAT receipts.

Step 7: Leverage Monthly Reporting for Business Insights

Though filing requires careful data tracking, it also provides valuable snapshots of your business activity. CFOs and accounting managers can use these insights to:

Forecast Cash Flow

- Compare monthly gross sales to expenses to identify emerging trends faster. For instance, if you notice a consistent uptick in input VAT, you might evaluate supplier costs or consider adjusting prices if expenditures seem too high.

Fine‑Tune Pricing or Spending

- Higher‑than‑expected VAT bills may indicate overspending or missed cost‑saving opportunities. By examining monthly summaries, your team can pinpoint inefficiencies - like excessive inventory - and respond quickly.

Assess Growth Readiness

- If you’re expanding or exploring new markets, monthly returns help you detect changes in revenue almost in real time. For example, a sudden spike in sales volumes could validate new product lines and guide further investment.

- The UK Office for National Statistics cites how monthly VAT data can refine GDP measurement; similarly, your finance team can weigh month‑by‑month VAT data to improve operational forecasts.

Conclusion

VAT returns can provide a faster route to refunds, clearer insights, and tighter cash flow management. By making submissions part of your regular accounting schedule, you’ll keep your business in good standing with HMRC and maintain a clear view of your finances. Consistency and accuracy are what matter most – and they’re within easy reach when you plan ahead, put the right systems in place, and understand how to file monthly VAT returns effectively.