Non-EU Context: The UK and Global Sellers

Following Brexit, the United Kingdom is no longer part of the VIES system for services or domestic trade, though Northern Ireland retains a special status for goods under the protocol. For businesses trading with the UK, understanding the distinction between a "GB" VAT number and an EU VAT number is vital.

The UK market remains a powerhouse for consumption and trade. Data shows that UK total VAT receipts in 2024/25 were £171 billion, reflecting a robust commercial environment. A UK business will typically have a number starting with "GB" followed by nine digits. Verification of these numbers must be done through the UK government's specific online checker, as VIES will return an "invalid" result for GB codes.

For a deeper look at post-Brexit compliance and practical impacts on international sellers, visit End of Brexit Transition: 6 Main Changes for International Sellers.

The sheer density of the market is notable. The UK had 2,285,900 active VAT-registered traders in the 2024/25 period. For international companies selling into the UK, or UK companies selling into the EU, the requirement often involves holding multiple registrations. You might need a local registration in France to store goods there, a GB registration for sales in London, and an OSS registration for sales to consumers in Germany.

Navigating these dual regimes requires careful planning. Companies must track different thresholds, filing frequencies, and currency requirements. This complexity leads many organizations to seek specialized help to manage their portfolio of registrations.

Modern Compliance: OSS and IOSS Schemes

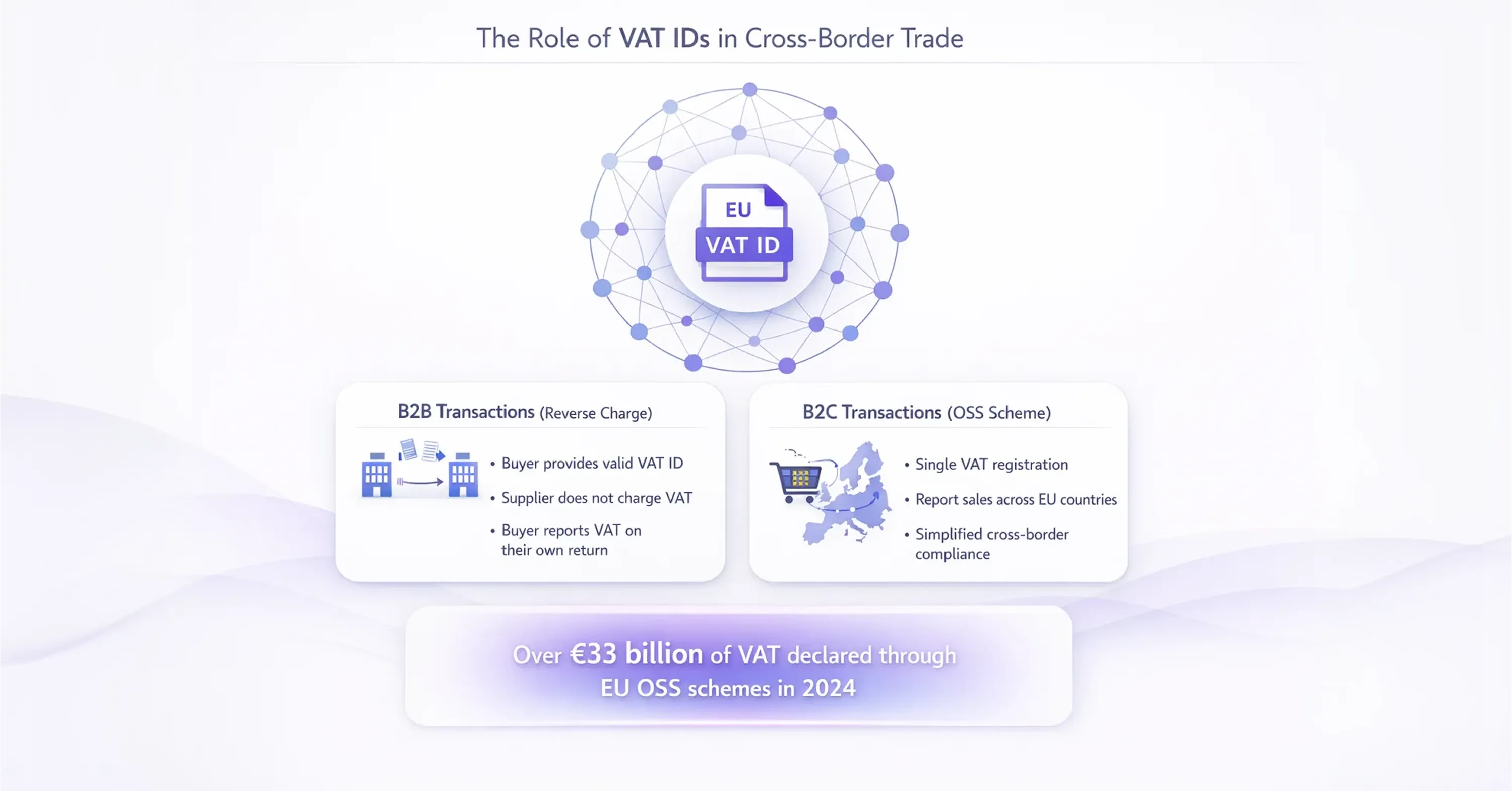

To reduce the administrative burden of holding multiple national VAT numbers, the EU introduced the One Stop Shop (OSS) and Import One Stop Shop (IOSS). These schemes allow businesses to register in just one Member State and declare all their pan-European sales via a single portal.

If you need a comprehensive comparison of EU VAT registration routes and what works best for your growth plan, see VAT in European Union: EU VAT Rules Explained for International Sellers.

The adoption of these simplified procedures has been rapid. By the end of 2024, over 170,000 traders had registered under the Union OSS, non-Union OSS, and Import OSS schemes. These systems are particularly valuable for e-commerce sellers importing low-value goods. In fact, VAT declared under the EU Import OSS scheme grew by 62% to €6.3 billion in 2024, proving that businesses prefer streamlined compliance over juggling dozens of local tax IDs.

However, "simplified" does not mean "simple." A business must still determine which scheme fits its model (Union vs. Non-Union), monitor turnover thresholds, and ensure data is aggregated correctly. Mismanagement here can lead to expulsion from the scheme, forcing the business back into the nightmare of registering in every single country where they have a customer.

For companies overwhelmed by the logistics of global expansion, 1StopVAT provides a comprehensive solution. Rather than relying on disparate local accountants, 1StopVAT offers a centralized team of certified tax specialists who manage registrations and filings across 100+ countries. Their approach combines necessary technology with human expertise to ensure that your use of OSS or local registrations aligns perfectly with current regulations.

Common Compliance Pitfalls and Solutions

Even with modern schemes like OSS, the "VAT Gap"—the difference between expected revenue and what is actually collected—remains a major issue for governments. The EU VAT compliance gap in 2022 was €89.3 billion, representing about 7% of total expected revenues. Authorities are closing this gap by enforcing stricter audits and penalties on businesses that make errors.

Electronic invoicing, digital recordkeeping, and knowing country-specific requirements have become crucial components of compliance. A detailed breakdown of pitfalls, including invoicing errors and missed deadlines—and how to proactively avoid them - is provided in How to Register for VAT in the EU: Step-by-Step Guide.

Common pitfalls include:

-

Incorrect Invoicing: Failing to quote the customer’s VAT number or using the wrong currency exchange rate.

-

Missing Deadlines: Each country has different filing dates (monthly, quarterly, or annual).

-

Ignoring Thresholds: Accidentally triggering a registration requirement in a new country by storing inventory there (e.g., using Amazon FBA).

The consequences of non-compliance range from heavy fines to the seizure of goods at the border. The complexity often arises when a business scales rapidly. A company might start selling only in Germany but suddenly find traction in Italy and Spain. Without a proactive strategy, they may unknowingly incur liabilities in those new jurisdictions.

For growing enterprises, partnering with a dedicated compliance firm is often safer than managing taxes in-house. 1StopVAT acts as a single point of contact for these expanding businesses, handling the intricate details of VAT registration and filing. Their team ensures that as you scale, your tax infrastructure scales with you, preventing the compliance gap from becoming a barrier to your success.

Conclusion

The European VAT number is more than just a requirement for paperwork; it is the passport for goods and services traveling across the EU single market. From the specific format of the ID to the daily necessity of verifying partners via VIES, understanding these elements protects your business from fraud and financial penalties.

As cross-border trade continues to grow, with billions of euros declared annually through streamlined systems like OSS, the mechanisms for compliance will likely become even more integrated. However, the fundamental responsibility remains with the trader to verify, report, and pay correctly. By maintaining rigorous verification standards and seeking expert support when operations become complex, businesses can navigate the European tax landscape with confidence and stability.