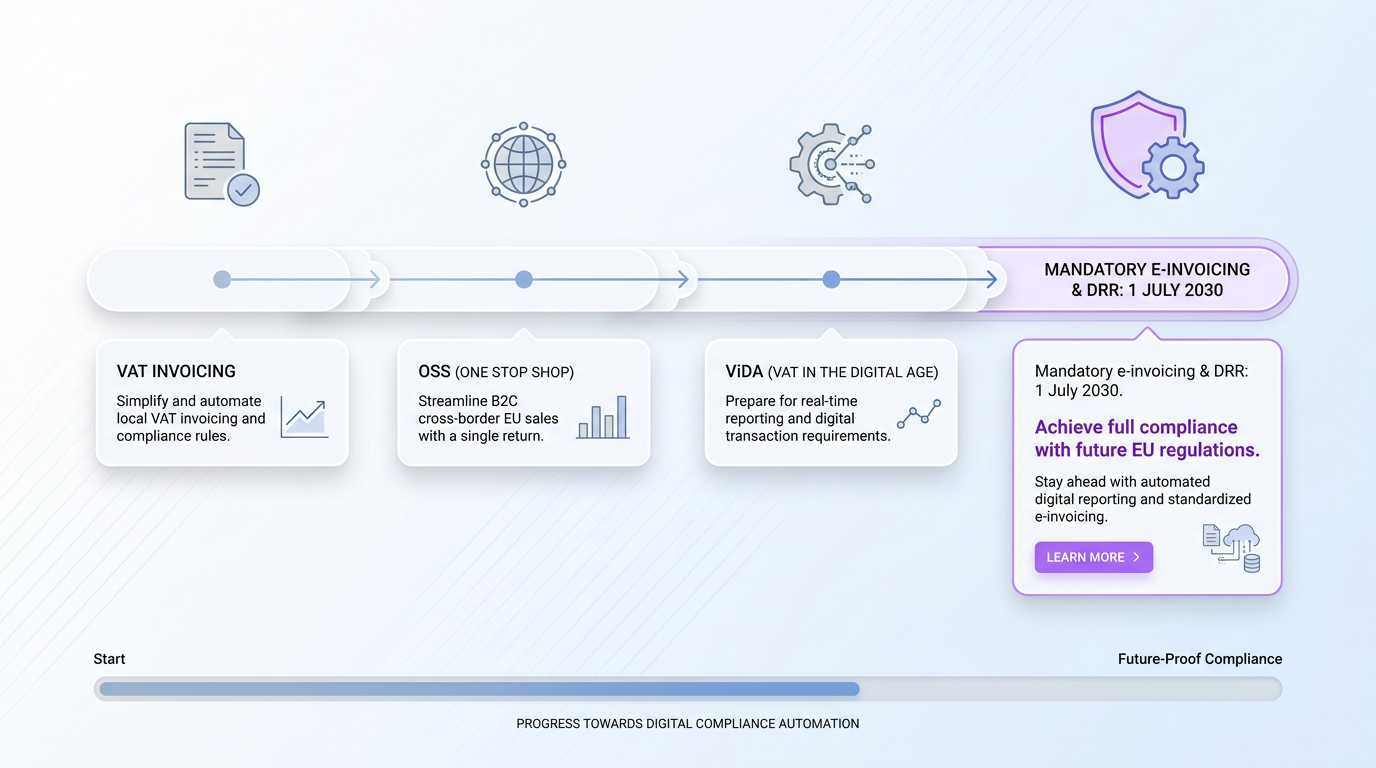

E-Invoicing Is Coming

The ViDA package introduces Digital Reporting Requirements (DRR) that will reshape how invoices are issued and transmitted. These requirements mandate e-invoicing and near real-time digital reporting for intra-EU transactions, effective from 1 July 2030. Several member states, including Italy, France, and Germany, are already implementing or planning national e-invoicing mandates ahead of that deadline.

If you're preparing for ViDA or want to understand upcoming e-invoicing rules and compliance essentials, see EU Invoicing Rules Explained for Businesses.

For SaaS businesses, this means invoice formats will need to follow structured electronic standards (like EN 16931) rather than simple PDF generation. Starting to plan for this transition now will prevent a scramble later. Companies that already generate invoices programmatically through their billing systems have a head start, but the compliance layer, ensuring the right fields, formats, and transmission protocols, still requires careful attention.

How ViDA Changes the Landscape Through 2035

The ViDA reforms go well beyond e-invoicing. The package aims to modernize the EU's VAT system, making it more resilient to fraud and addressing challenges raised by the development of the platform economy. For SaaS companies, three pillars matter most.

Single VAT Registration simplifies obligations further. Starting from 1 July 2028, reforms include mandatory reverse charge for non-identified suppliers, reducing the need for multiple country registrations in scenarios that currently require them.

Platform economy rules are also expanding. While most directly affecting short-term accommodation and transport platforms, the new rules make platforms facilitating certain services responsible for collecting and remitting VAT under certain conditions. SaaS companies that operate as marketplaces or facilitate third-party transactions should assess whether these deemed-supplier provisions apply to them.

The financial stakes are significant. The ViDA package is projected to help Member States collect up to €18 billion more in VAT revenues annually over a ten-year period, with €11 billion resulting from anti-fraud measures. That level of expected recovery signals increased enforcement and audit activity, giving SaaS companies every reason to get compliance right now.

Staying Compliant Without Building an In-House Tax Team

Many SaaS companies, especially those in growth stages, don't have dedicated tax departments. Yet the obligations described above demand consistent attention: verifying customer locations, applying correct rates, filing returns on time, and adapting to regulatory changes across dozens of jurisdictions.

This is where working with a specialized VAT compliance partner makes a real difference. Top Companies for Digital Services VAT Compliance provides in-depth reviews of providers who can handle everything from VAT registration to ongoing filings and audits. 1StopVAT, for example, combines a team of over 40 certified tax specialists with coverage across 100+ countries, acting as a single point of contact for VAT registration, filing, and consulting. For SaaS companies selling into the EU, having that kind of dedicated guidance means you can focus on your product while the compliance side is handled by people who track these regulatory shifts daily.

A practical example: a US-based SaaS company launching in Europe might start with the non-Union OSS, then expand into direct registrations as enterprise B2B contracts grow. A compliance partner like 1StopVAT can manage both tracks, ensuring invoices meet local requirements and filings stay current as the ViDA timeline unfolds.

Conclusion

EU VAT compliance for SaaS companies in 2025 comes down to a few core disciplines: correctly identifying customer location with documented evidence, choosing the right registration path, issuing compliant invoices, and preparing for the structural changes ViDA will bring over the next decade. None of these steps are optional, and together they form a continuous obligation rather than a one-time setup. As SaaS companies grow across Europe, VAT becomes part of everyday operations, affecting pricing, billing, subscription management, and customer onboarding. Even small compliance gaps, such as incorrect VAT rates or unverified customer information, can quickly turn into larger financial and regulatory risks.

With ViDA introducing more automated reporting and e-invoicing requirements, EU tax enforcement is moving toward greater transparency and real-time oversight. SaaS businesses that build scalable VAT processes early, whether through automation or specialized compliance support, will be far better positioned to expand smoothly across European markets.

The companies that treat VAT as part of their long-term growth strategy rather than a reactive obligation are the ones most likely to scale confidently, avoid costly disruptions, and maintain trust with customers and regulators alike.