Step 5: File and Pay VAT Accurately

Electronic service tax compliance hinges on timely returns. Missing a deadline can bring interest and reputational damage.

Filing frequency and deadlines

- OSS: quarterly, due by the end of the month following the reporting quarter

- Union Member States outside OSS: monthly or quarterly

- Non-EU countries:

- Japan: monthly, quarterly, or yearly

- South Africa: bimonthly or monthly

Learn more about digital filing, automation, and country-specific requirements in How to File VAT Returns Online: Streamlining Digital Submission.

Practical reporting tips

- Automate data extraction from payment gateways into a VAT report template.

- Double-check the currency conversion rate used on the day of supply.

- Pay via SEPA or local tax authority’s portal to avoid bank fees.

EU Member States lost about €89 billion in VAT in 2022, roughly 7% of revenue. Closing that gap is a political priority, so expect stricter audits. Getting your returns right the first time keeps you off the radar.

Step 6: Maintain Records and Stay Audit Ready

Auditors can request transaction evidence up to ten years after the sale. Prepare now rather than scramble later.

- Store invoices, payment receipts, and location evidence in a secure archive.

- Use a consistent file naming convention: YYYY-MM client-name invoice-number.

- Review VAT codes in your billing system quarterly to catch rate changes.

- Document your place-of-supply logic and any manual overrides.

Keep an eye on rate updates and legislative changes. Globally, 101 countries now tax cross-border online sales. A quick internal checklist review every six months prevents surprises.

Step 7: Know When to Seek Expert Help

Rapid expansion can stretch an in-house finance team thin. A specialist firm such as 1stopVAT, with over 40 certified tax advisers covering 100-plus countries, can handle VAT registration, ongoing compliance, and complex advisory while you focus on product growth. Whether you need a second opinion on OSS filings or a full outsourced solution, external guidance often costs less than one major penalty.

For tips on weighing in-house work vs. outsourcing - and the specific value a VAT specialist can deliver - refer to VAT Compliance & Consultancy: Why Expert Advice Matters.

A final thought before moving on: Engage experts early if you plan to enter multiple new markets in one quarter, launch marketplace sales, or change your business model from licensing to subscription.

Digital services VAT compliance means charging the correct VAT rate where the customer is located, registering through schemes like the EU One-Stop Shop once you pass the €10 000 threshold, issuing invoices with mandatory details, filing returns on time, and storing records for up to ten years.

Conclusion

VAT rules for digital services evolve quickly, but a structured approach keeps you compliant. Confirm thresholds, register through schemes like OSS, issue accurate invoices, file on time, and archive everything. When resources tighten, consider partnering with experienced advisers such as 1stopVAT. Follow these steps and you can expand globally while keeping VAT headaches to a minimum.

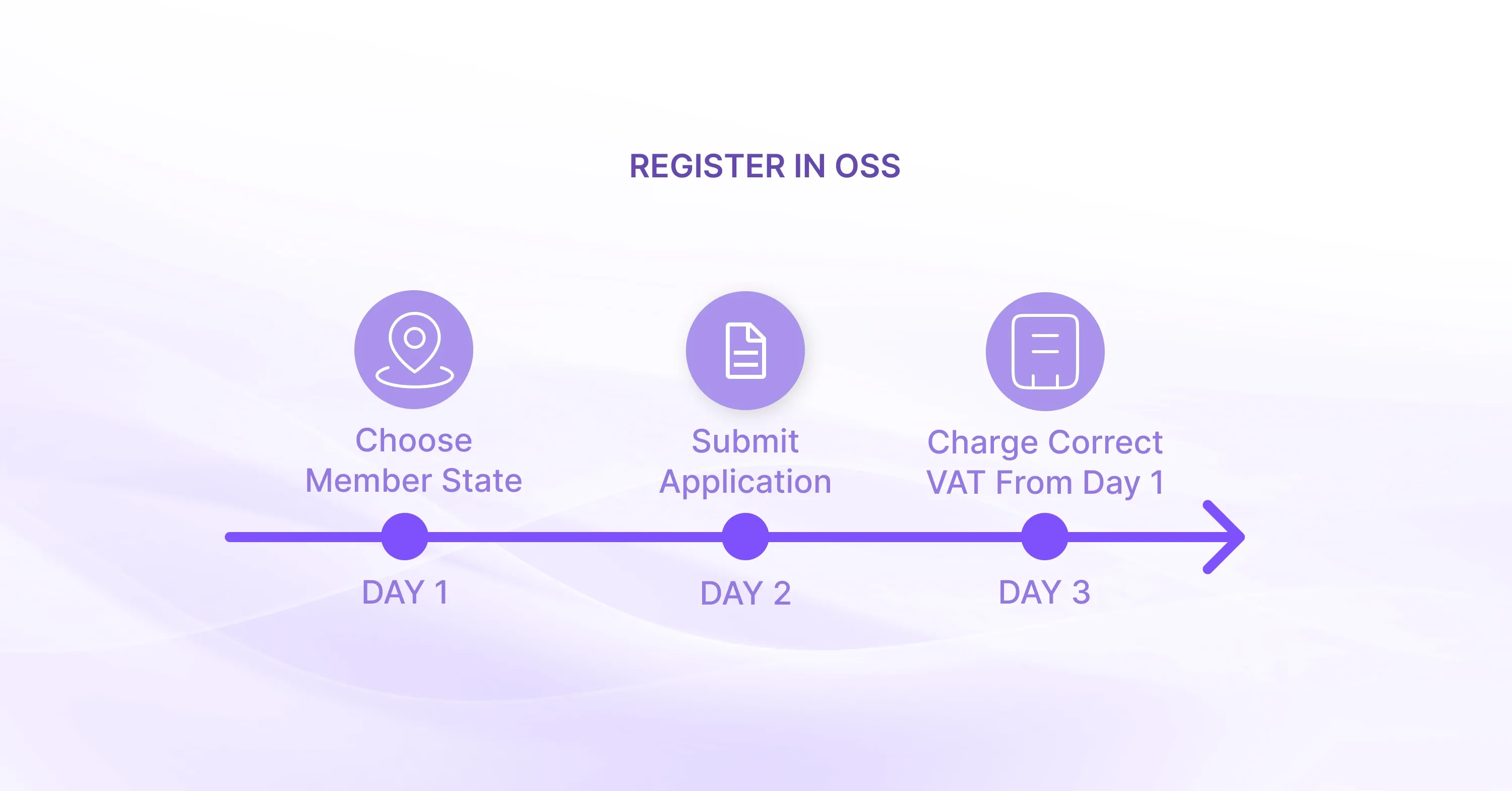

Once you exceed the EU threshold or decide to charge VAT voluntarily, the OSS scheme becomes your best friend. You register once in a single EU Member State, file one quarterly return, and authorities distribute the tax to each country.

Once you exceed the EU threshold or decide to charge VAT voluntarily, the OSS scheme becomes your best friend. You register once in a single EU Member State, file one quarterly return, and authorities distribute the tax to each country.