Build a Compliance Calendar and Monitor Changes

E-invoicing regulations across the EU are still evolving. Deadlines shift, technical specifications get updated, and new countries announce mandates. A static compliance strategy won't work.

Build a living compliance calendar that tracks:

-

Country-specific go-live dates for mandatory e-invoicing

-

Transition periods and grace periods (like Germany's phased approach through 2027)

-

Format and platform updates from tax authorities

-

ViDA legislative milestones as they progress through EU institutions

Assign ownership internally. Someone in your finance or tax team needs to monitor regulatory updates from national tax authorities and the European Commission regularly.

For businesses operating in many EU markets, this monitoring burden grows quickly. A marketplace seller listing products in Germany, France, Italy, and Poland, for example, faces four different e-invoicing regimes with different timelines, formats, and reporting obligations.

This is where most businesses start making expensive mistakes - trying to manage four different e-invoicing regimes with internal resources that weren't built for this. 1StopVAT works with businesses that operate across multiple EU markets and can't afford compliance gaps. Their team monitors regulatory changes across 100+ countries in real time, so when Poland moves its KSeF deadline or France updates its PDP requirements, your invoicing process adjusts - before it breaks. For marketplace sellers managing VAT registration, compliance filings, and e-invoicing across jurisdictions simultaneously, that's not a convenience.

Test, Validate, and Go Live Before Deadlines Hit

Don't wait until a mandate's effective date to switch systems. Most countries offer pre-mandate testing periods, and using them is critical.

Run parallel invoicing during your transition phase:

-

Issue invoices in both your old format and the new structured format

-

Validate e-invoices against the EN 16931 schema before transmitting

-

Test connections to government platforms using sandbox or pilot environments

-

Verify that your trading partners can receive and process your e-invoices

A common real-world issue: a German wholesaler discovered during testing that its ERP system was omitting the buyer's VAT registration number from the structured XML output. That single missing field caused every test invoice to be rejected by the validation service. Catching this months before the mandate saved significant disruption.

Early testing also gives your accounting and finance teams time to adjust workflows. E-invoicing changes how invoice disputes, credit notes, and corrections are handled, and staff need to understand the new processes before they're mandatory.

To stay compliant with EU e-invoicing regulations, businesses must issue invoices in structured electronic formats (UBL or CII) conforming to the EN 16931 standard, connect to required government platforms in each EU country where they operate, and meet country-specific deadlines ranging from 2024 (Romania) to 2030 (ViDA's EU-wide cross-border mandate).

Common E-Invoicing Challenges Businesses Encounter During Implementation

In practice, many businesses discover that e-invoicing compliance issues rarely come from misunderstanding the legislation itself. The bigger challenge is adapting internal workflows, ERP configurations, approval chains, and reporting processes to meet different country-specific technical requirements at the same time.

For example, companies rolling out e-invoicing across Germany, France, Poland, and Italy often face inconsistencies between local platform requirements, invoice validation rules, and structured XML field mappings. Even small configuration gaps, such as missing VAT identifiers or incompatible invoice syntax, can lead to invoice rejection and reporting delays.

Conclusion

The businesses that will struggle most with EU e-invoicing aren't the ones who don't understand the regulations. They're the ones who understood them too late to adapt their systems, retrain their teams, and fix the configuration gaps before the first rejected invoice. Every country on this list has a deadline. Several of them have already passed.

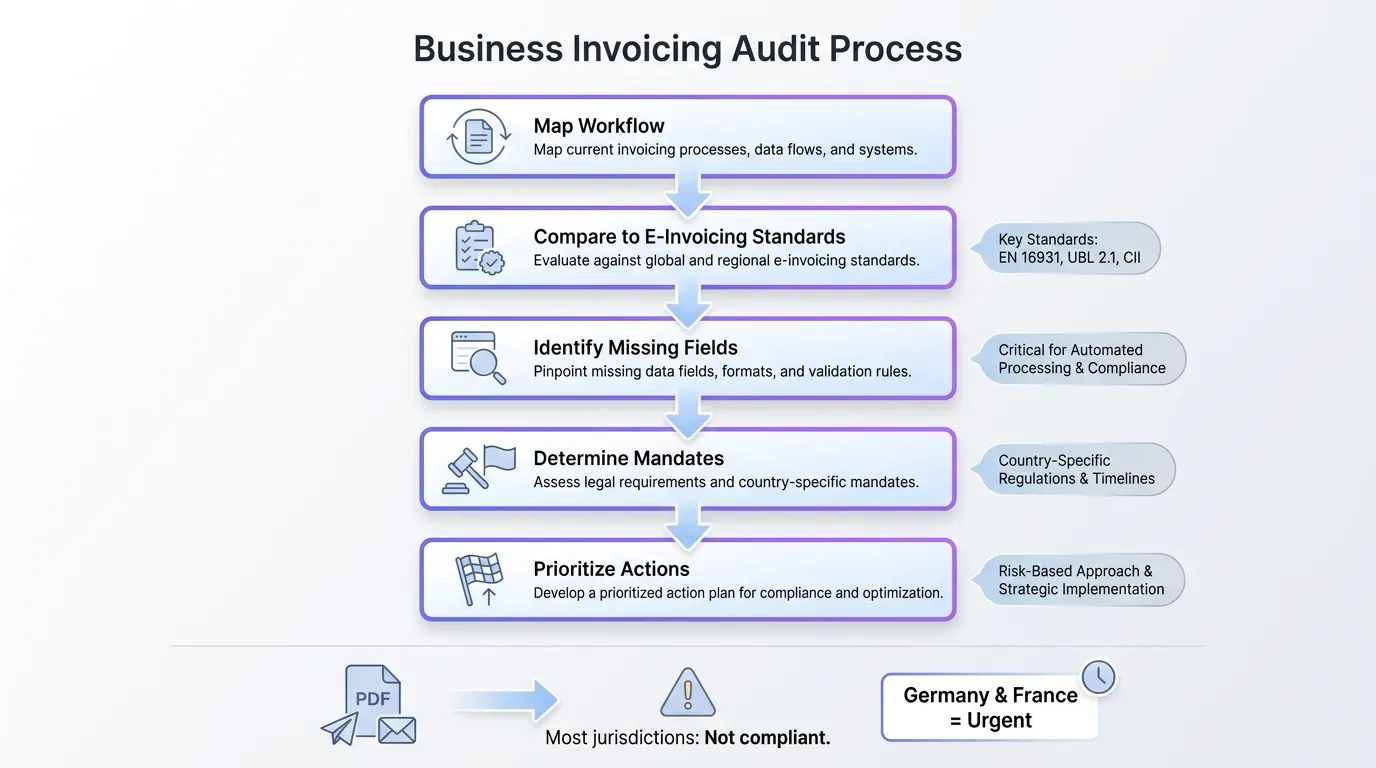

If you're operating across EU markets and haven't mapped your current invoicing setup against the requirements above, that's the first thing to do today - not next quarter. Audit your formats, check your ERP output, confirm which government platforms apply to each market you invoice into.

If you want a clear picture of where your compliance stands and what needs to change, talk to the 1StopVAT team. They cover 100+ countries and can help you identify gaps before they become compliance issues.