Navigate the Approval Timeline

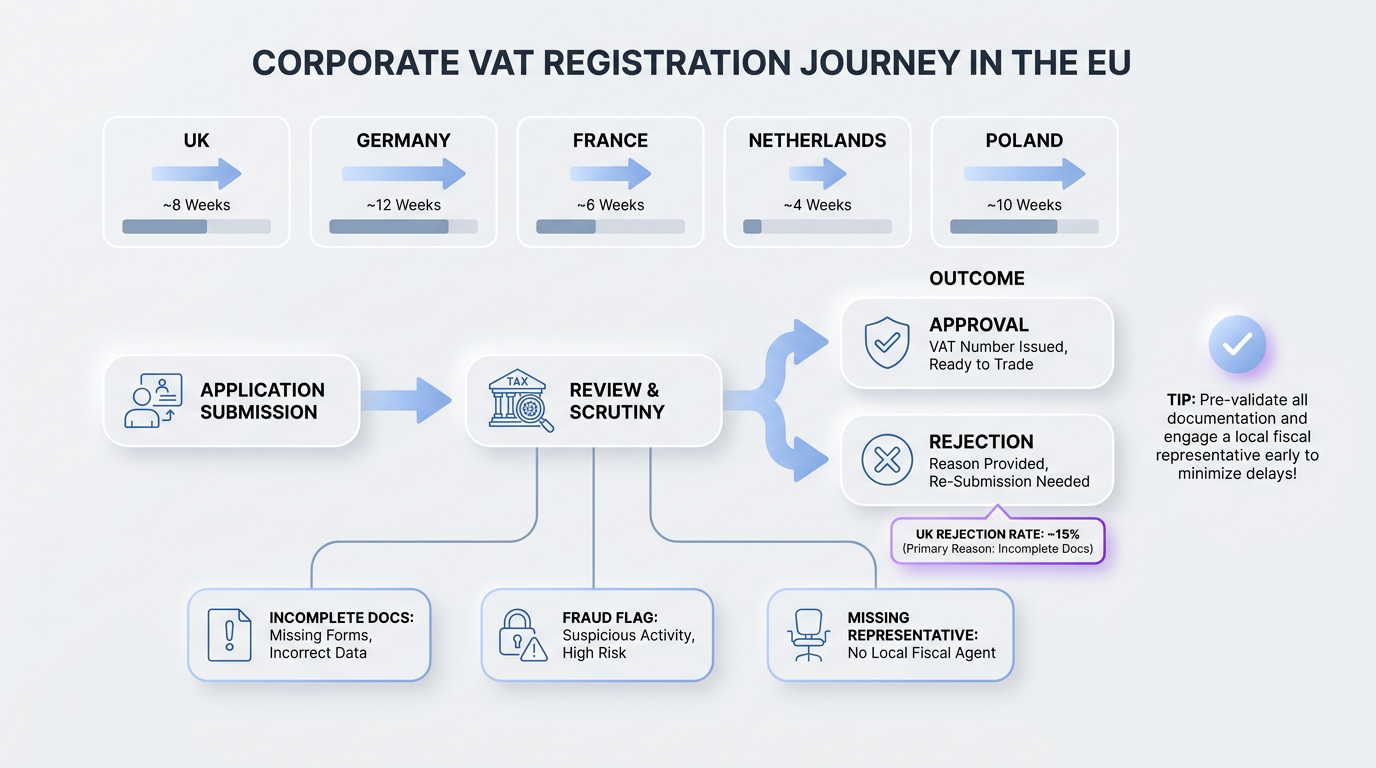

Timelines for receiving your corporate VAT number differ widely depending on the country and the completeness of your application. Setting realistic expectations here prevents unnecessary stress and helps you plan your operations accordingly.

Typical processing times:

-

UK (HMRC): 30 business days for standard online applications; up to 3 months for complex or flagged cases

-

Germany: 4 to 8 weeks, sometimes longer for non-EU applicants

-

France: 2 to 6 weeks with a fiscal representative in place

-

Netherlands: 2 to 4 weeks for EU companies; longer for non-EU

-

Poland: up to 2 months, with additional verification steps common

What causes delays

Tax authorities commonly request additional information mid-process, which resets the clock. The most frequent causes include:

-

Incomplete or inconsistent documentation

-

Mismatch between declared business activity and submitted evidence

-

Missing fiscal representative where one is legally required

-

Applications flagged for fraud checks

In the UK specifically, HMRC has increased scrutiny in response to VAT fraud, contributing to that 17% rejection rate in 2024. Over 50,000 applications were refused or withdrawn. Many of these weren't fraudulent; they were simply incomplete or poorly supported.

To avoid unnecessary delays, consult the VAT Tax Registration: Complete Step-by-Step Guide for checklists and common mistakes that could impact your approval timeline.

Respond promptly to any queries from the tax authority and keep copies of every submission. This diligence shortens the approval window and brings you closer to your active VAT status.

Set Up Compliance from Day One

Receiving your VAT number isn't the finish line. It's actually the starting point for ongoing obligations. The moment your registration is active, you're required to charge VAT correctly, maintain records, and file returns on schedule.

Your immediate post-registration checklist should include:

-

Update invoicing systems to include your new VAT number and apply correct rates

-

Confirm your filing frequency, whether monthly, quarterly, or annually

-

Set calendar reminders for return deadlines and payment due dates

-

Establish record-keeping procedures that meet local retention requirements (usually 6 to 10 years)

A real-world scenario: a UK e-commerce company received its VAT number but failed to update its checkout system for three weeks. During that period, it collected payments without charging VAT, creating an immediate liability it had to absorb from its margins.

The scale of VAT collected through compliant systems continues to grow rapidly. In 2024, over €33 billion in VAT revenues were collected via the EU's e-commerce VAT systems, a 26% increase over 2023. Tax authorities are investing heavily in digital reporting, which means errors are caught faster than ever.

For practical guides on digital record-keeping, filing deadlines, and multi-country compliance, see VAT Filing & Returns: A Complete Guide for Businesses and VAT Compliance Services for Shopify and WooCommerce Stores.

For companies managing VAT across multiple jurisdictions, partnering with a specialist provider like 1StopVAT ensures filings are accurate and deadlines are met, combining human expertise with streamlined processes to keep you fully compliant as you scale internationally.

What Is Company VAT Registration?

Company VAT registration is the formal process by which a business registers with a tax authority to collect and remit Value Added Tax. It involves determining registration obligations, submitting an application with supporting documents, receiving a unique corporate VAT number, and maintaining ongoing compliance through periodic filings. Registration may be mandatory (when turnover exceeds a threshold) or voluntary (to reclaim input tax).

Conclusion

Company VAT registration is a structured process, but it demands attention to detail at every stage. From confirming your obligations and assembling thorough documentation to submitting a complete application and setting up compliance systems immediately, each step builds on the last. The businesses that get it right the first time are the ones that treat registration not as an administrative chore, but as foundational infrastructure for growth. As 2.73 million VAT-registered businesses in the UK demonstrate, proper VAT registration is simply part of doing business at scale. Whether you're expanding into new markets, selling through international marketplaces, or managing cross-border operations, VAT compliance directly affects invoicing, cash flow, customer trust, and long-term operational stability.

The reality is that VAT obligations rarely become simpler as a business grows. New sales channels, additional countries, inventory storage arrangements, and evolving digital reporting rules all increase complexity over time. Companies that build strong compliance processes early are far better positioned to scale internationally without disruptions, penalties, or unnecessary administrative overhead.