Real-World Example: Selling Into Multiple Markets

A mid-sized electronics seller based in China lists products on Amazon (EU), eBay (UK), and a local Norwegian marketplace. Under EU rules, Amazon collects VAT on imported goods up to €150. In the UK, eBay handles VAT on consignments up to £135. In Norway, the seller may need to register for VOEC (VAT on E-Commerce) if the marketplace doesn't handle the obligation. Three markets, three sets of rules, three potential registration requirements.

This is where online marketplace VAT gets genuinely complicated. Each country's rules interact differently with the platform's policies, and a seller's obligations shift depending on where inventory is stored, where the customer is located, and whether the platform qualifies as a deemed supplier in that jurisdiction.

For a more detailed breakdown of multi-jurisdictional VAT requirements and practical comparison of available compliance schemes - including when the OSS or IOSS can replace multiple national registrations - consult the VAT Tax Registration: Complete Step-by-Step Guide.

Navigating this patchwork is why many growing sellers turn to specialists like 1StopVAT, whose team of 40+ certified tax professionals provides tailored guidance and filing support across these varied regulatory environments.

Staying Compliant as Rules Continue to Evolve

Marketplace VAT rules aren't static. The EU is already working on "VAT in the Digital Age" (ViDA) proposals, which will expand platform obligations further, introduce real-time digital reporting, and tighten rules around deemed supplier transactions. For an in-depth explanation of the EU's digital-age reforms and how they’ll impact your processes, see VAT in the Digital Age: How Could it Affect Your Business?.

The UK is reviewing its own framework post-Brexit. And countries across Asia-Pacific are steadily introducing new marketplace collection models.

For sellers and platforms alike, the path forward involves:

-

Monitoring regulatory changes in every market where you sell or store goods.

-

Maintaining clean data, because accurate product classifications, customer locations, and transaction records are the foundation of compliance.

-

Choosing the right compliance support, whether in-house tax teams or external partners who specialize in cross-border ecommerce tax compliance.

For further reading on how external experts can help centralize and streamline your cross-border VAT filings, see Top VAT Firms for Online Marketplaces.

An ecommerce marketplace becomes responsible for collecting and remitting VAT under the EU's "deemed supplier" model when it facilitates sales of imported goods valued up to €150, or sales by non-EU sellers from EU-based inventory. Sellers retain obligations for VAT registration where they store goods, intra-EU stock movements, and B2B transactions.

The growth of marketplace commerce shows no signs of slowing. Mirakl-powered marketplace sales grew by 53% year-over-year during Cyber Week 2022, dramatically outperforming the 2% growth of overall ecommerce during the same period. As marketplaces capture more of the retail economy, VAT compliance will only become more central to how sellers and platforms operate.

Conclusion

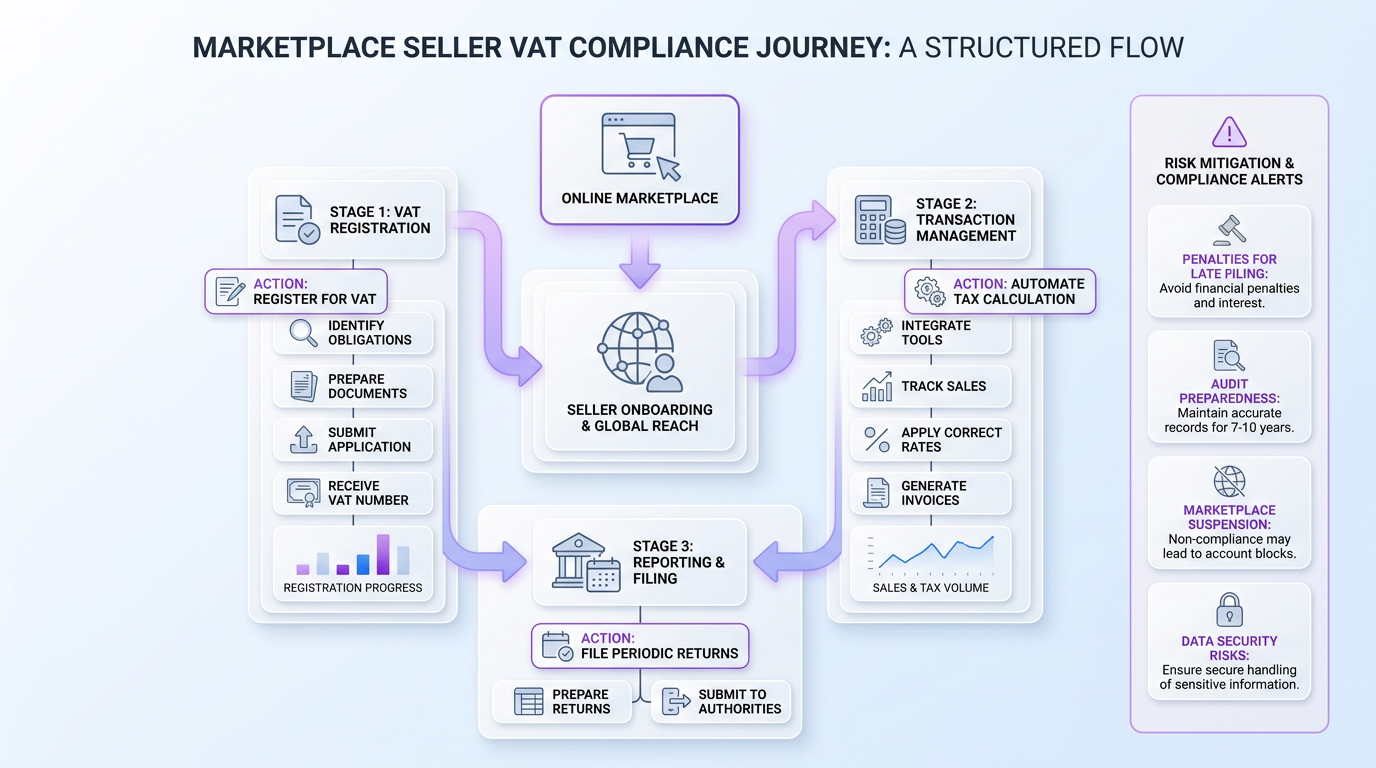

VAT rules for ecommerce marketplaces have fundamentally reshaped how tax is collected on online sales, shifting critical responsibility onto platforms while leaving sellers with complex, non-obvious obligations. The deemed supplier model simplifies part of the process, but it doesn’t eliminate the need for VAT registrations, inventory tracking, and accurate reporting across multiple jurisdictions. For cross-border sellers, this is where compliance often breaks in practice. Different thresholds, country-specific rules, and evolving regulations create a fragmented landscape where even small oversights can lead to audits, penalties, or operational disruption.

Staying compliant today requires more than a basic understanding of VAT rules. It demands structured processes, reliable data, and a clear view of where your obligations actually arise. In a marketplace-driven economy, VAT compliance isn’t just a back-office task. It’s a critical part of protecting your revenue, maintaining platform access, and scaling your business without costly setbacks.