Overview

Making Tax Digital (MTD) for VAT is now a mandatory requirement for all VAT-registered businesses in the UK, fundamentally changing how VAT records are kept and returns are submitted. Instead of manual processes, businesses must use digital record-keeping systems and MTD-compatible software to ensure accurate, real-time reporting to HMRC.

This guide explains what MTD VAT means in practice, who must comply, how digital record-keeping works, and what software solutions are available. It also covers the latest rules, submission process, and penalties for non-compliance, helping you stay fully aligned with UK VAT regulations.

What MTD VAT Actually Means

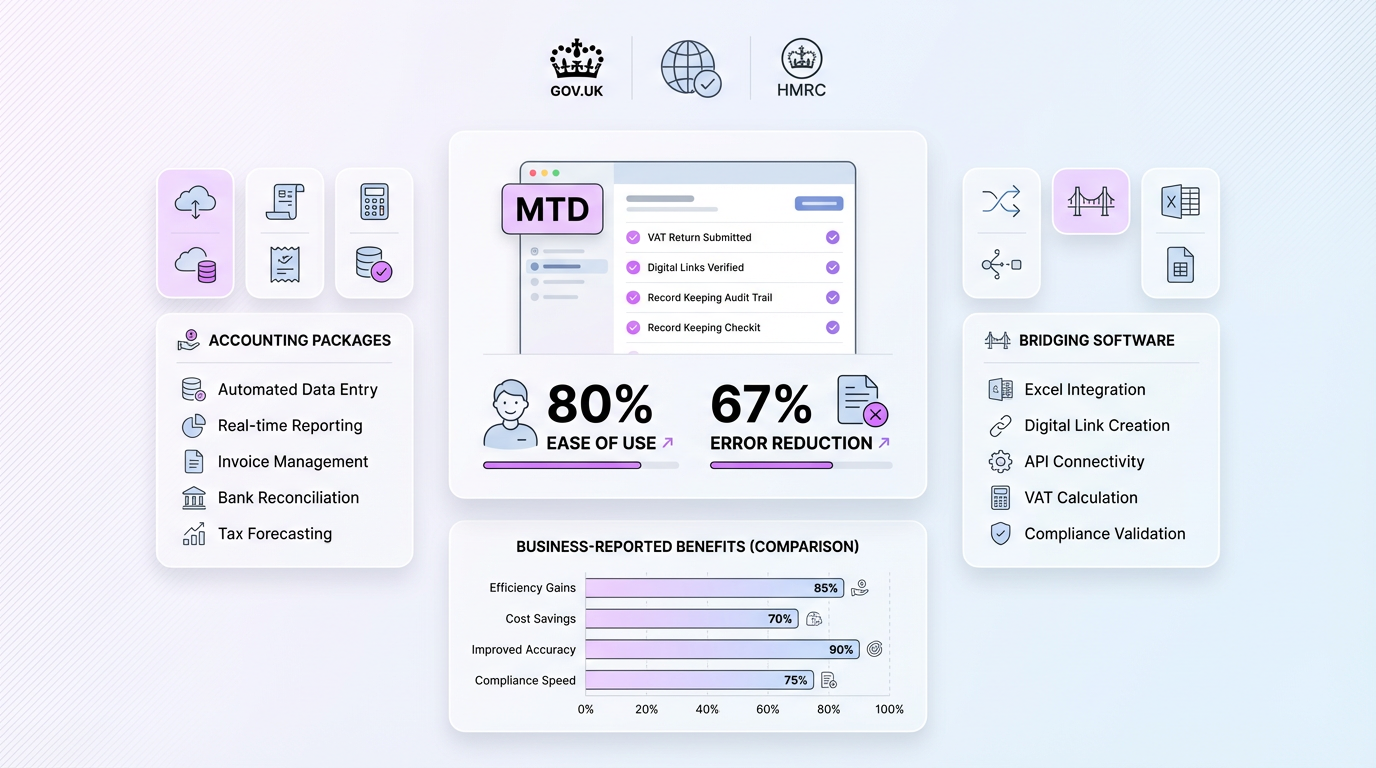

Making Tax Digital for VAT is HMRC's initiative to modernize the UK tax system by requiring businesses to keep digital records and submit VAT returns through compatible software. The goal is straightforward: fewer errors, more accurate reporting, and a tax system that works in real time rather than relying on manual paperwork.

The programme launched in April 2019. That first phase applied to VAT-registered businesses above the £85,000 threshold, totaling 1.2 million businesses. Since April 2022, MTD VAT has been mandatory for all VAT-registered businesses, regardless of turnover. If you're registered for VAT, you're in scope.

Here's what MTD VAT requires in simple terms:

-

You must keep your VAT records digitally (not on paper ledgers or non-compliant spreadsheets).

-

You must submit your VAT returns using MTD-compatible software, not through HMRC's old online portal.

-

Any transfer of data between software programs must happen through digital links, not manual re-keying.

This shift from paper to digital VAT reporting is the core of the entire programme, and it touches every part of how you record, calculate, and submit your VAT. For a comprehensive breakdown of best practices and step-by-step prep, see Accurately Filling Out a VAT Return.

Who Needs to Comply

Understanding whether MTD VAT applies to you is simpler than it used to be, because the answer today is: almost everyone.

If your business is VAT-registered in the UK, you must follow MTD rules. This includes sole traders, partnerships, limited companies, and overseas businesses registered for UK VAT. The only exemptions are narrow and typically involve religious objections, disability, or remote locations where internet access isn't feasible. HMRC grants these on a case-by-case basis.

For marketplace sellers operating across borders, MTD VAT adds another layer to an already complex compliance landscape. If you sell through platforms like Amazon or eBay into the UK and hold a UK VAT registration, you're subject to the same digital record-keeping and filing obligations as domestic businesses. That's where working with a specialist matters. 1StopVAT, for instance, provides dedicated VAT filing and guidance for marketplace sellers navigating obligations across multiple countries, acting as a single point of contact backed by over 40 certified tax specialists.

Digital Record-Keeping Rules

Now that you know who's covered, the next question is: what counts as "digital records" under MTD?

HMRC doesn't prescribe one specific format. However, your digital records must include certain mandatory information:

-

Your business name, address, and VAT registration number

-

The VAT accounting scheme you use

-

The VAT rate charged on each supply

-

The time of supply (tax point) and the net value of the transaction

-

The total output tax and input tax for each return period

You can still use spreadsheets, but only if they're linked digitally to your submission software. Manual copy-pasting numbers from a spreadsheet into a VAT return doesn't meet the standard. The "digital links" requirement means data must flow electronically from your record-keeping tool to your filing tool without human re-entry.

For a detailed look at how digital records and backup practices fit the broader submission process, check Accurately Filling Out a VAT Return.