Submit and track your VAT number registration

After submission, the portal issues an acknowledgement reference. HMRC, for example, asks applicants not to chase the status until 40 working days have passed. Other authorities are faster: the Netherlands issues a VAT number within two weeks for straightforward applications, while Germany takes six to eight weeks because of additional anti-fraud checks.

If the authority asks for more information, respond through the portal rather than by email. Upload the requested document with a short note about what it shows, then confirm receipt. A partial rejection is rarely the end of the road. It signals one specific gap, and once that gap is closed, registration for VAT continues from where it stopped. A full rejection is rare and means the applicant didn't qualify because the trading activity is exempt or the entity isn't yet incorporated.

While you wait, you can continue trading. You cannot yet show a VAT number on invoices, but you can raise prices to cover the VAT that will eventually be due and reissue corrected invoices once the number arrives.

After you receive your VAT number

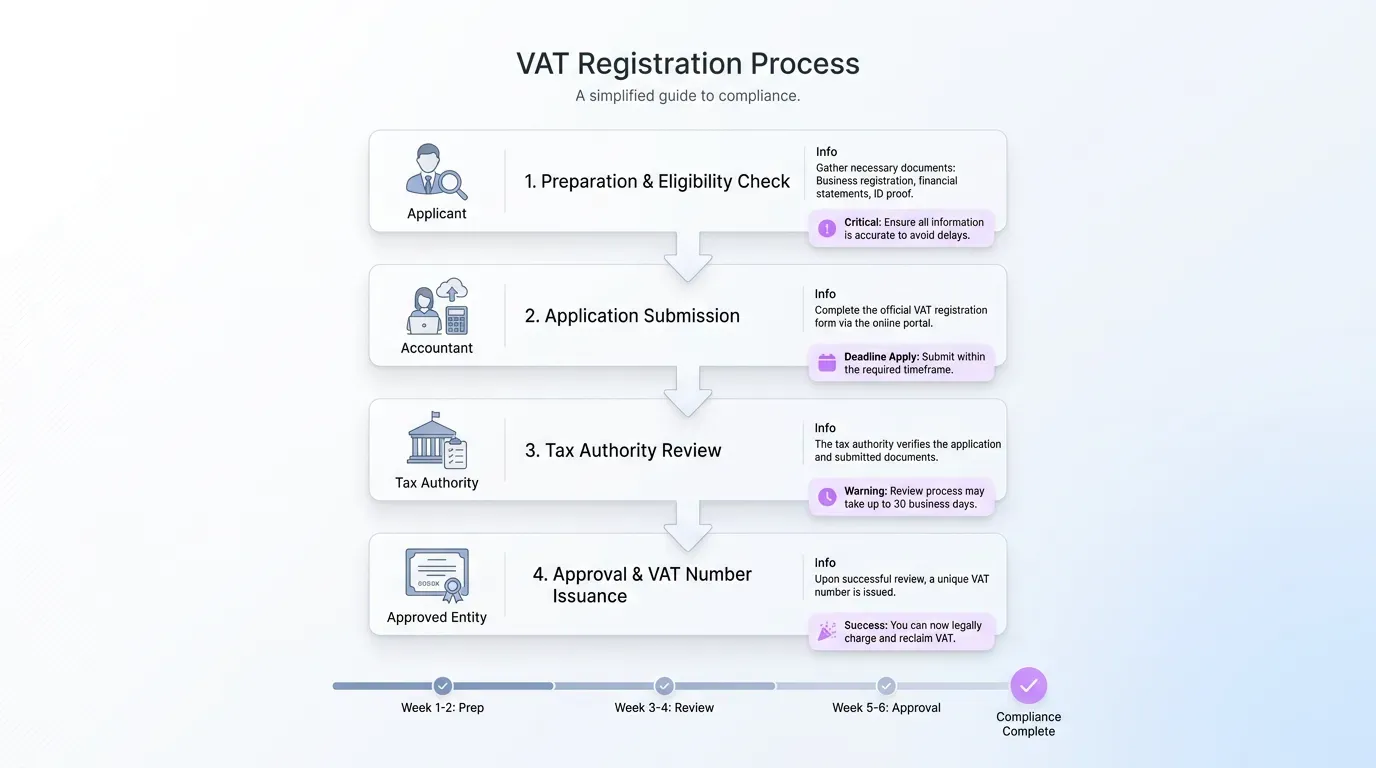

The VAT number registration certificate lands by post or as a downloadable PDF in your tax account. Read it carefully. It confirms the details of your registration for VAT: your number, the effective date of registration, the filing frequency, and the date your first return is due.

The immediate tasks are practical:

-

Update invoice templates to show the VAT number and the VAT amount on each line at the VAT rate applied.

-

Add the number to your website footer and any marketplace seller profiles, and update your terms of service too.

-

Configure accounting software (Xero, QuickBooks, Sage, or whatever you use) to apply the right rates and produce a return in the format your authority accepts.

-

Reissue any invoices raised between your effective date of registration and the date the number arrived so they show the VAT that was always due.

Displaying the number correctly matters. EU customers will check it against the VIES database before paying, and a missing or invalid number can hold up settlement. The certificate marks the beginning of compliance.

Ongoing duties and common mistakes

A VAT-registered business has recurring duties: charge the correct rate on every taxable sale and file returns on time, with records that prove both. In the UK you must keep VAT records for at least 6 years, or 10 years if you use the One Stop Shop. The EU One Stop Shop also requires records to be held for 10 years from the end of the year of the transaction.

The mistakes that catch new registrants are predictable. Missing a return deadline is the most expensive. HMRC's points-based regime issues a £200 penalty once a business reaches the threshold for its filing frequency, plus a further £200 for each subsequent late submission. Misclassifying zero-rated and exempt items is the second trap, because the two look similar but behave differently when you reclaim input VAT. Treating reverse-charge supplies as standard-rated, or the other way around, distorts the return and triggers correction notices.

A few habits keep most businesses out of trouble:

-

Reconcile sales and purchase ledgers monthly rather than scrambling at quarter-end.

-

Use Making Tax Digital-compatible software in the UK, or the equivalent e-invoicing platform in countries that mandate one.

-

Set calendar reminders for the return deadline and the payment deadline, which can differ by a few days.

-

Engage a VAT adviser whenever you start selling into a new country or change your business model.

Paul Riley, Director of Tax Administration at HMRC, framed the points regime this way when it launched: "Our aim is to help customers get things right before monetary penalties are applied; a points-based system for late VAT returns will not punish the occasional error." The system is forgiving of one slip and unforgiving of repeated ones.

Next steps and final tips

Registration for VAT is administrative work. Confirm whether you must register or want to register voluntarily, collect your documents, set up the tax account, fill in the form, and respond quickly to any follow-up questions. Bookmark this guide and prepare your folder before you begin the application when your numbers and paperwork agree.

If your situation involves multiple countries or marketplace sales, especially when an activity sits on the edge of an exemption, talk to an accountant or call your local tax authority before submitting. A 30-minute conversation is cheaper than a corrected return.

1stopVAT handles registration for VAT and ongoing compliance across more than 100 jurisdictions, with return filing covered for international businesses. If your VAT application process touches more than one country or you'd like a second pair of eyes on your VAT number registration before you submit, reach out to our team for a consultation.