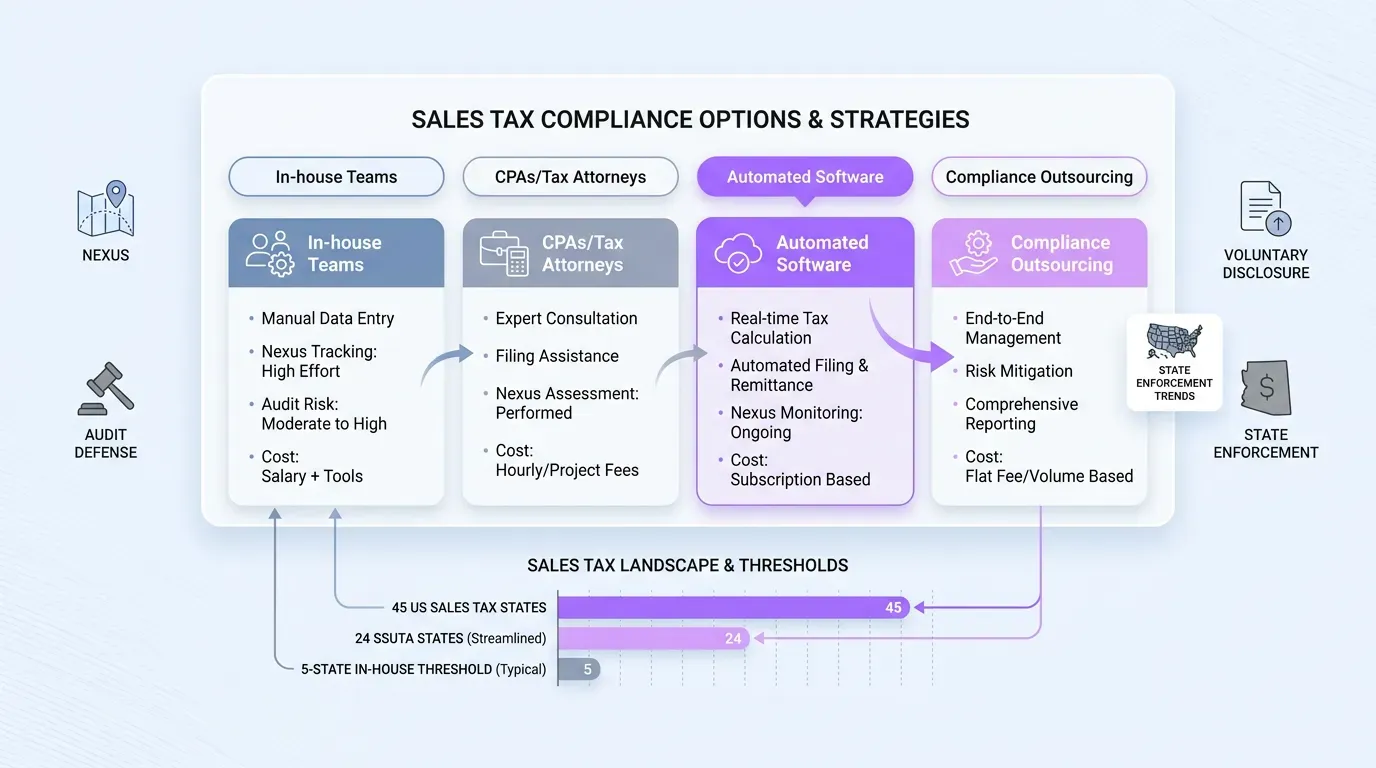

Which option fits which type of business?

The right handler depends on the seller's nexus footprint, transaction volume, product mix, and international expansion plans. Domestic sellers with light nexus can manage with software. Sellers in 10 or more states, or those crossing borders, benefit from a managed compliance partner.

The Bloomberg Tax survey found that the number of states with economic nexus more than doubled within a year of the Wayfair decision, and the total jumped to 33 states by May 2019. The pace of that expansion is what makes any "set it and forget it" approach risky. A business that fits the software profile this quarter can outgrow it next quarter without realizing it. Reviewing handler fit annually, against current nexus data and growth plans, keeps the compliance model aligned with where the business actually sits.

When is software alone enough?

Software alone is enough for purely domestic sellers with stable nexus in fewer than five states and a single product category, with a finance team comfortable reading state notices. The numbers stay manageable and the software's filing automation does the heavy lifting.

The OECD's 2018 simplified registration report noted only 3,777 sellers had registered under SSUTA's simplified regime as of late 2017, a thin uptake that suggests most growing sellers don't stop at the lightweight option. If the catalog is stable and the states are few, software keeps overhead low when the team has bandwidth, without buying capacity nobody uses.

When do you need a managed service?

A managed service becomes necessary once a business crosses nexus in 10 or more states, sells digital products with shifting taxability, faces state notices regularly, or expands outside the US. At that point, the volume of recurring work exceeds what a finance team can carry without hiring.

The Wayfair ruling expanded sales tax obligations rapidly across the country, and as the OECD noted in its 2024 Consumption Tax Trends, every one of the 45 states with sales taxes has adopted remote seller collection rules. A managed provider absorbs that scope as a service line. The implication for finance leaders is practical: at the 10-state mark, the cost of a managed service is less than the salary of the half-FTE you would otherwise hire to keep up.

How does US sales tax connect to global VAT and GST?

US sales tax connects to global VAT and GST through the same underlying obligation: registration where you sell and collection at the right rate, followed by remittance to the local authority. Businesses selling internationally face parallel obligations under EU and UK VAT and Canadian and Australian GST, with similar regimes across the rest of the world.

The OECD reports that VAT has been implemented in 175 countries worldwide and now operates in 37 of the 38 OECD member countries, with the United States as the lone exception. A US-based seller shipping to Germany hits EU VAT rules. A European seller hitting California's $500,000 threshold owes US sales tax. The two systems collide constantly for cross-border e-commerce, and a registration strategy that ignores one side leaves the other exposed.

Why split US and international compliance across vendors?

Splitting US and international compliance across separate vendors creates blind spots and duplicated data entry, and it slows responses to nexus triggers in either region. It also produces two reporting cadences that finance teams have to reconcile manually.

When a seller crosses the EU's distance selling threshold in the same quarter it crosses Texas's $500,000 threshold, a single provider catches both. Two providers each catch one. The OECD's Consumption Tax Trends 2024 shows VAT raising about a fifth of total tax revenue across the OECD, which is why authorities globally have invested heavily in enforcement against non-resident sellers. Splitting compliance across providers raises the probability that one of those enforcement letters lands before the seller knew the threshold was approaching.

What does unified indirect tax compliance look like?

Unified indirect tax compliance means one provider managing US state registrations, EU One Stop Shop (OSS) filings, UK VAT, Canadian and Australian GST, and other regimes through a single account team and reporting cadence. The seller sees one dashboard and one point of contact, with a consolidated calendar behind both.

The Bhutan GST launch in 2026 added another jurisdiction to the global map, according to VATabout's 2026 indirect tax review, while Liberia is preparing to replace its GST with a VAT system in 2027. New regimes appear every year. A unified model means new-country expansion gets added to an existing service line, which avoids a fresh vendor search and keeps cross-border growth from stalling on compliance setup.

How 1stopVAT handles multi-state registration and global compliance

If you've read this far, you already know that the operational choice is who runs the registration process. 1stopVAT is built for businesses that need US sales tax registration and international VAT and GST compliance handled by one accountable partner.

Here is what the service covers in practical terms:

-

Sales tax registration across all US states starting at $250 per state

-

Ongoing return filings from $99 per return, including state notice handling

-

Continuous nexus monitoring across more than 12,000 US local jurisdictions

-

VAT and GST registration and filings in 100+ countries, including the EU OSS, UK VAT, and Canadian and Australian GST

The team has 40+ certified tax specialists working across US sales tax and international indirect tax, so US-only sellers get the same depth of support as cross-border ones. If your business is approaching nexus in new states or expanding into Europe, talk to 1stopVAT for a scoping call and a fixed-price proposal aligned to your current footprint; the same process applies if you are already juggling two compliance vendors.