Country of origin and trade agreements

Where goods are manufactured affects the rate as much as what they are. Preferential trade agreements lower or eliminate duty on qualifying goods that meet the agreement's rules of origin. Under the United States-Mexico-Canada Agreement (USMCA), qualifying goods move duty-free between the three countries. The Comprehensive Economic and Trade Agreement (CETA) made 98% of tariff lines duty-free at entry into force, and that share rose to 99% by January 2024. The EU-Japan Economic Partnership Agreement eliminated 99% of EU tariff lines and 97% of Japan's at entry into force.

To claim the lower rate, you need proof of origin in the form of a certificate or self-declaration from the exporter that meets the agreement's documentation rules. Without it, customs applies the most-favored-nation rate by default. The EU's overall MFN average for all goods sits at 5.2% in 2023, while the US average was 4.8%, so the gap between preferential and standard treatment is the difference between a thin margin and a profitable one.

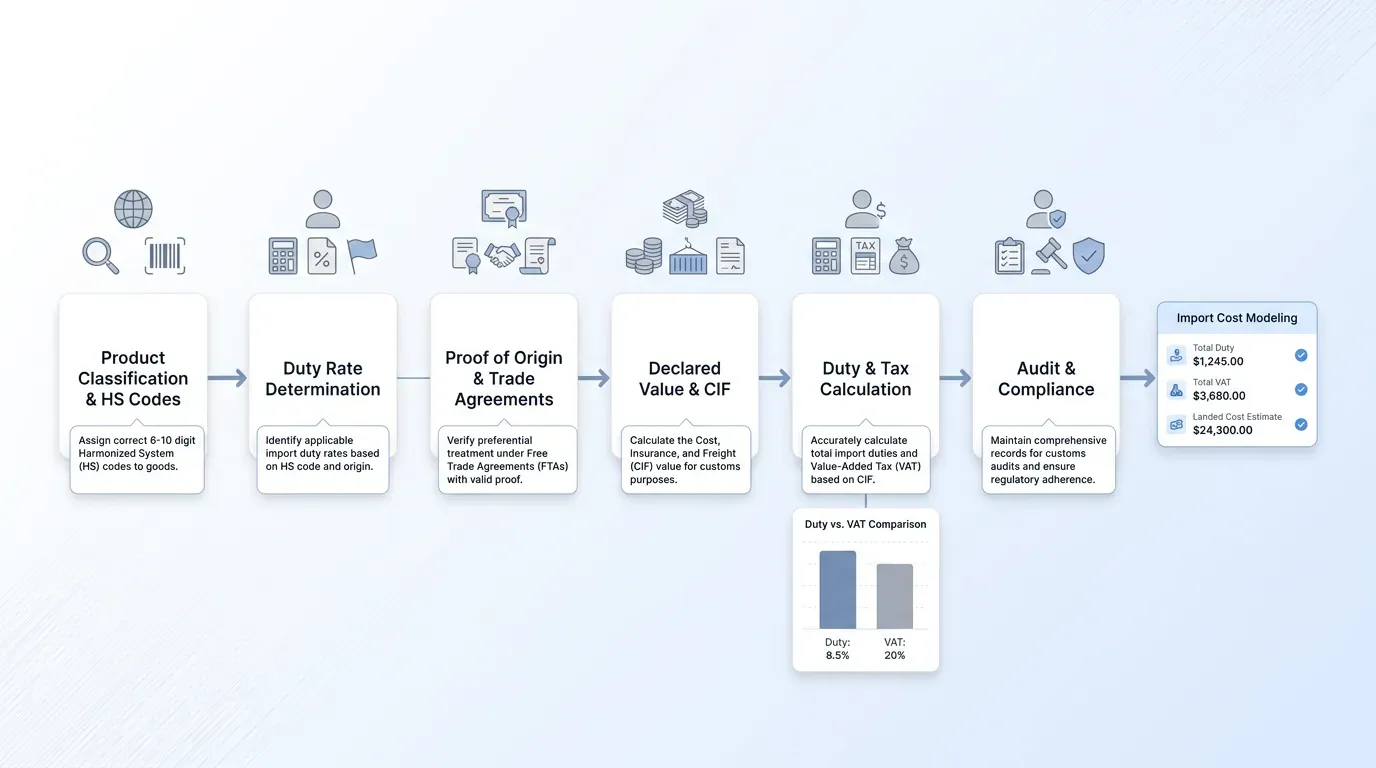

Customs duty calculation and declared value

Customs duty calculation starts with the declared customs value. For most countries this is the Cost, Insurance and Freight (CIF) value, which is the price paid for the goods plus insurance and freight to the border. The duty rate from the tariff schedule is then applied to that base.

A simple worked example: a 5% duty rate on a $10,000 CIF shipment produces $500 in duty. If the rate were 12%, the same shipment would owe $1,200. The percentage looks small until you multiply it across a year of containers.

Undervaluing goods to reduce duty is illegal and audited heavily. The EU's anti-fraud office identifies mis-declaration of value as one of the main fiscal customs fraud types, alongside misclassification and false origin. Customs authorities cross-check declared values against transactional databases, so the short-term saving rarely survives a post-clearance audit.

Additional taxes and import tax rules

Duty is rarely the only charge. Import tax rules in most countries add VAT or GST, plus processing or handling fees on top of the duty, with excise added on certain categories. These charges are calculated separately on the duty-inclusive value, which compounds the cost.

UK guidance is explicit on this point. When goods enter Northern Ireland and are deemed at risk of onward movement, VAT is calculated on the customs value including any duties due. The same logic applies in most EU member states and many other jurisdictions. A 20% VAT rate applied to a duty-inclusive value adds meaningfully more than 20% of the original goods price.

The practical effect: when you compare landed costs across suppliers or routes, you must model the full border charge because VAT or GST and any country-specific fees change the total. Looking at the duty line alone hides up to two-thirds of the import tax rules that determine your final cost.

A simple duty calculation example

Walk through a realistic scenario for customs duty calculation. A UK retailer imports 1,000 units of a cotton t-shirt from a supplier in Bangladesh. At $8 per unit, the invoice totals $8,000; freight to the UK port is $1,200 and insurance is $300.

Step 1: confirm the HS code. Cotton t-shirts fall under HS heading 6109. The retailer checks the UK Global Tariff and finds a duty rate of 12% applies to non-preferential origins.

Step 2: calculate the CIF customs value.

Step 3: apply the duty rate. 12% of $9,500 = $1,140 in import duty.

Step 4: calculate VAT. UK standard VAT is 20%, charged on the CIF value plus duty. That base is $9,500 + $1,140 = $10,640. VAT due is $2,128.

Step 5: total landed tax cost. Duty of $1,140 plus VAT of $2,128 equals $3,268 in border charges on a $9,500 shipment. The full landed cost, before domestic logistics, is $12,768. If the same shirts came from a country with a UK preference agreement and the documents were in order, the duty line would drop to zero and pull total border charges down to $1,900 in VAT only.