Step 4: Double-Check for Special Transactions

- Reverse charge services (standard in cross-border services)

- Imports and exports that might trigger postponed VAT accounting

- Hire purchase or lease agreements

- Partial exemption methods

Pro Tip

When preparing a VAT return, early review of unusual transactions like imports subject to reverse charge is critical. This will ensure consistent monthly records and save you from confusion over filing time.

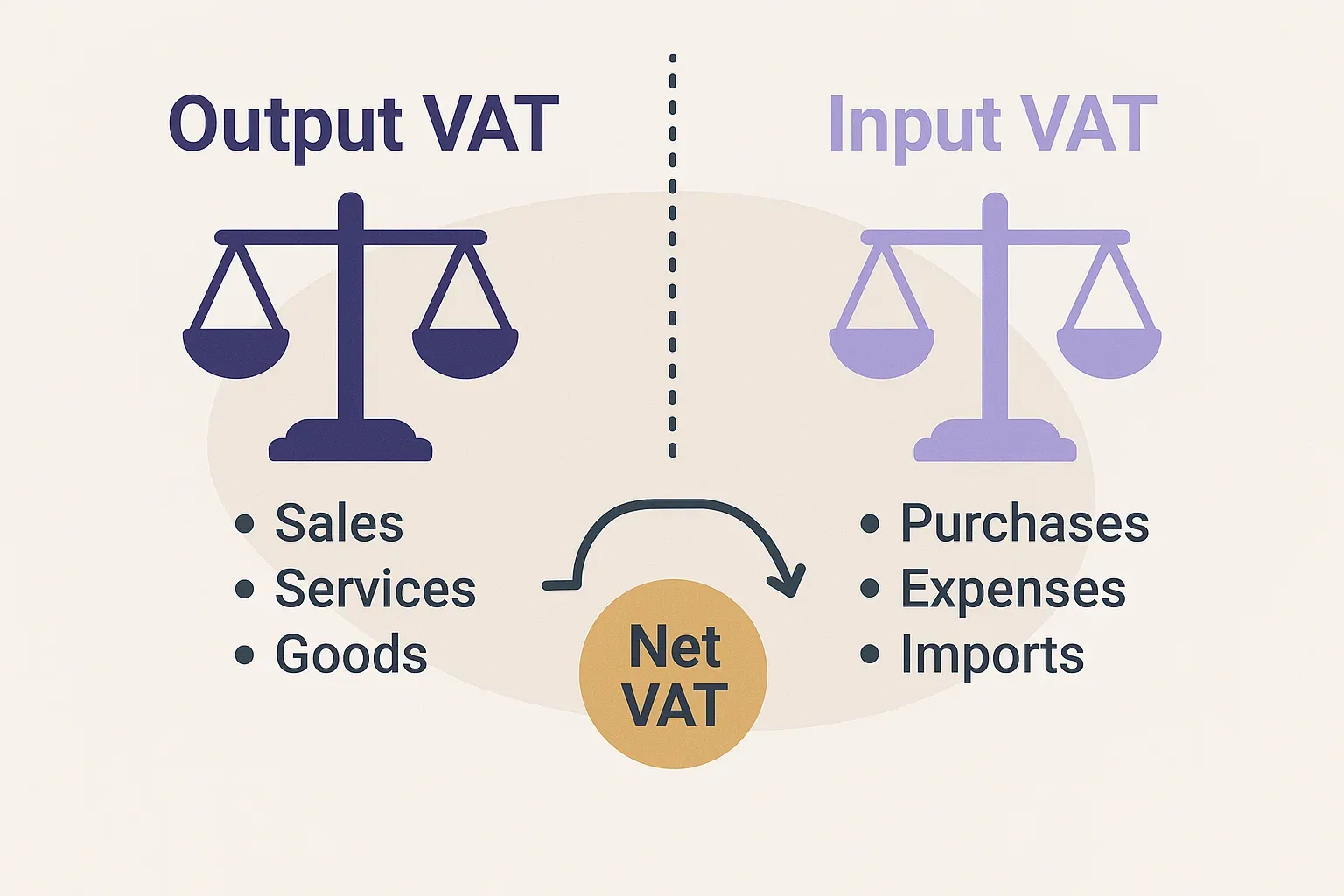

Step 5: Complete the Return Fields Carefully

Your VAT return usually includes:

- Total sales and purchases (boxes 6 and 7 on the UK VAT form)

- Output VAT due (box 1)

- Input VAT claimable (box 4)

- Net liability (box 5)

Enter each figure cautiously, especially if you handle multiple currencies:

- Consider any adjustments for errors in previous returns.

- Watch out for the correct decimal places - tiny errors can escalate.

Businesses risk higher penalties once their data is repeatedly inaccurate.

Step 6: Submit Your VAT Return Digitally

Submitting your VAT return digitally each period helps ensure accuracy and compliance with HMRC requirements. Aim to file well before the due date to avoid last-minute issues.

To stay on track:

-

Use an officially recognised digital submission method.

-

File early to prevent surcharges or penalties from late submissions.

-

Keep complete digital transaction records for audit purposes, in line with MTD requirements.

Step 7: Record Your Confirmation and Payment

Once the filing is over, you’ll receive a confirmation. Preserve it in your records.

Prompt payment of any outstanding VAT balance is crucial:

- Arrange a direct debit for regular auto-payments if it suits your setup.

- If you spot an error, alert HMRC quickly to avoid interest charges.

- Plan for each VAT period’s potential liabilities in your cash flow forecast.

This way, you’ll avoid underpayments or late payments and save your business from any extra fees.

Conclusion

Filling in a VAT return with sufficient preparation reduces risks and increases trust in your data. From collecting complete records to verifying special transactions, every step ensures cleaner data and fewer headaches. Investing extra effort in VAT return accuracy helps businesses avoid costly mistakes and overpayments. By following our comprehensive checklist for completing a VAT return and referring to trusted resources, you’ll be ready to file with confidence and accuracy.