Overview

We will unpack the key components of VAT and sales tax in international trade, explain when and where a foreign company must register, and clarify emerging rules for digital services. You will also learn how to synchronize filings across several jurisdictions, keep audit-ready records, and choose outside help when internal capacity runs thin. By the end, you will have a clear blueprint to scale globally, implement global tax solutions, and sleep well during tax season.

Understand VAT and Sales Tax in International Trade

Indirect taxes look similar at first glance but vary widely in scope, rate, and collection mechanics. Getting the basics right avoids cascading errors later.

VAT vs. Sales Tax: A Quick Primer

Value Added Tax applies at every stage of the supply chain, with businesses offsetting input VAT against output VAT. Sales tax, common in the United States, is charged only at the final sale to consumers. Roughly 170+ countries run a VAT system, while fewer than 30 rely primarily on sales tax.

- VAT is destination-based: the tax belongs where the customer consumes the good or service.

- Sales tax is origin-based within the US: the seller collects based on the buyer’s state and local rates.

- Imports are usually taxable, exports often zero-rated, yet documentary proof is essential.

Many firms misapply domestic concepts abroad, leading to double taxation. A strong grasp of these contrasts is the first pillar of international VAT compliance. For a more detailed comparison, see the Sales Tax Registration and Compliance Guide for Global Sellers.

Ending this section, remember: treat each country’s VAT or sales tax as unique, not a copy-paste exercise. Next we explore when you must register.

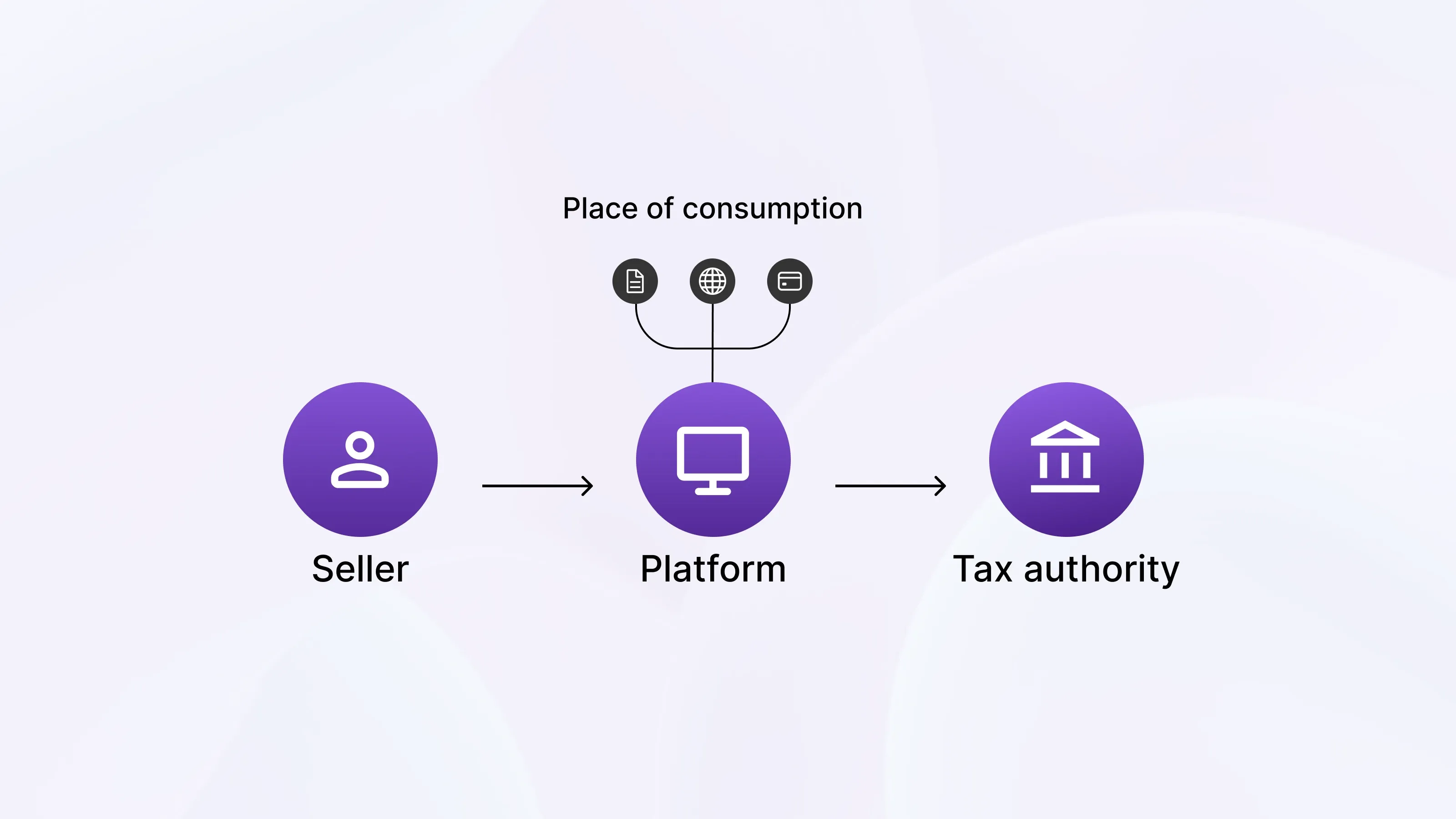

Registration Requirements for Foreign Sellers

Cross-border transactions often create “taxable presence” long before a legal entity exists in the target country.

Foreign companies must register when they either hold stock locally or cross a revenue threshold. In the EU, registration can trigger at €0 if you store goods in a member state’s warehouse. Meanwhile, Australia and Norway require VAT registration once digital revenue to consumers exceeds AU$75,000 and NOK 50,000 respectively.

Identify thresholds:

- Physical goods: distance-selling limits in the EU, state nexus rules in the US.

- Digital services: often lower or nil thresholds.

Gather documents early: certificate of incorporation, bank letters, passport copies of directors.

Expect variations in processing time:

- Germany, 6–8 weeks

- Singapore, 10 working days

Delay costs money. For example, 55 % of importers reported customs holds due to missing VAT IDs last year. Filing before your first shipment avoids storage surcharges.

In many cases, external advisors streamline multi-country registrations. Firms such as 1stopVAT act as a single point of contact, sparing finance teams from tracking a dozen portals and languages. For benchmark thresholds and compliance checklists, see the VAT Compliance Checklist for Startups and Small Businesses.

Now that you are registered, let’s tackle the complexities of digital services taxation.