Step 5: Report Accurately and On Time

Don't let tax deadlines catch you by surprise. While the tax world might seem like a predictable calendar of April 15ths, the reality is far more complex.

Depending on where you operate, the type of tax you're dealing with, and even the volume of your business transactions, a multitude of deadlines could be lurking just around the corner. Missing even one can lead to significant financial penalties and headaches.

- Use a master calendar with color-coded urgency levels.

- Automate reminders escalating to senior management at minus five days.

- File electronically where possible to gain instant confirmation.

Penalty matrix for non-local businesses

For non-local businesses, tax compliance can feel like a high-stakes game of chess—one wrong move triggers costly consequences. Rules vary widely across jurisdictions, where a small oversight in one country may result in severe penalties in another. Our Penalty Matrix for Non-Local Businesses highlights the key financial risks to help you stay ahead and protect your bottom line.

-

Late filings: percentage of tax due or flat daily amounts

-

Underpayments: interest plus surcharges up to 50%

-

Non-registration: trading bans, customs holds, reputational damage

Here’s how global sellers benefit from a step-by-step approach to registration, reporting, and compliance.

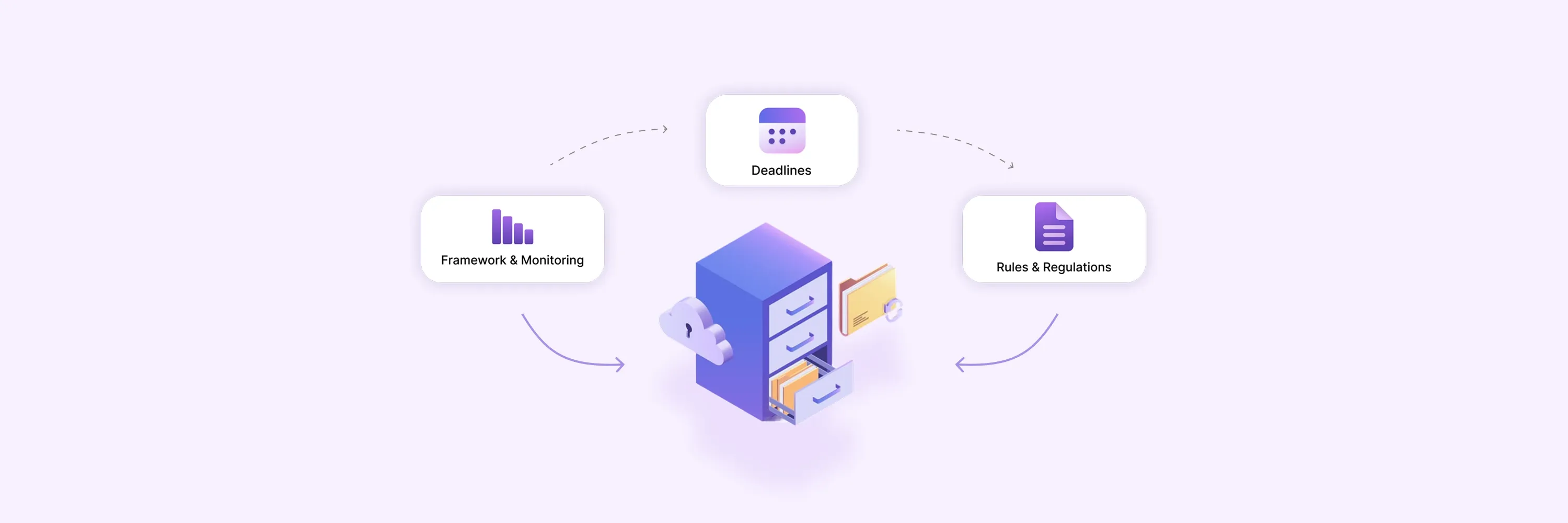

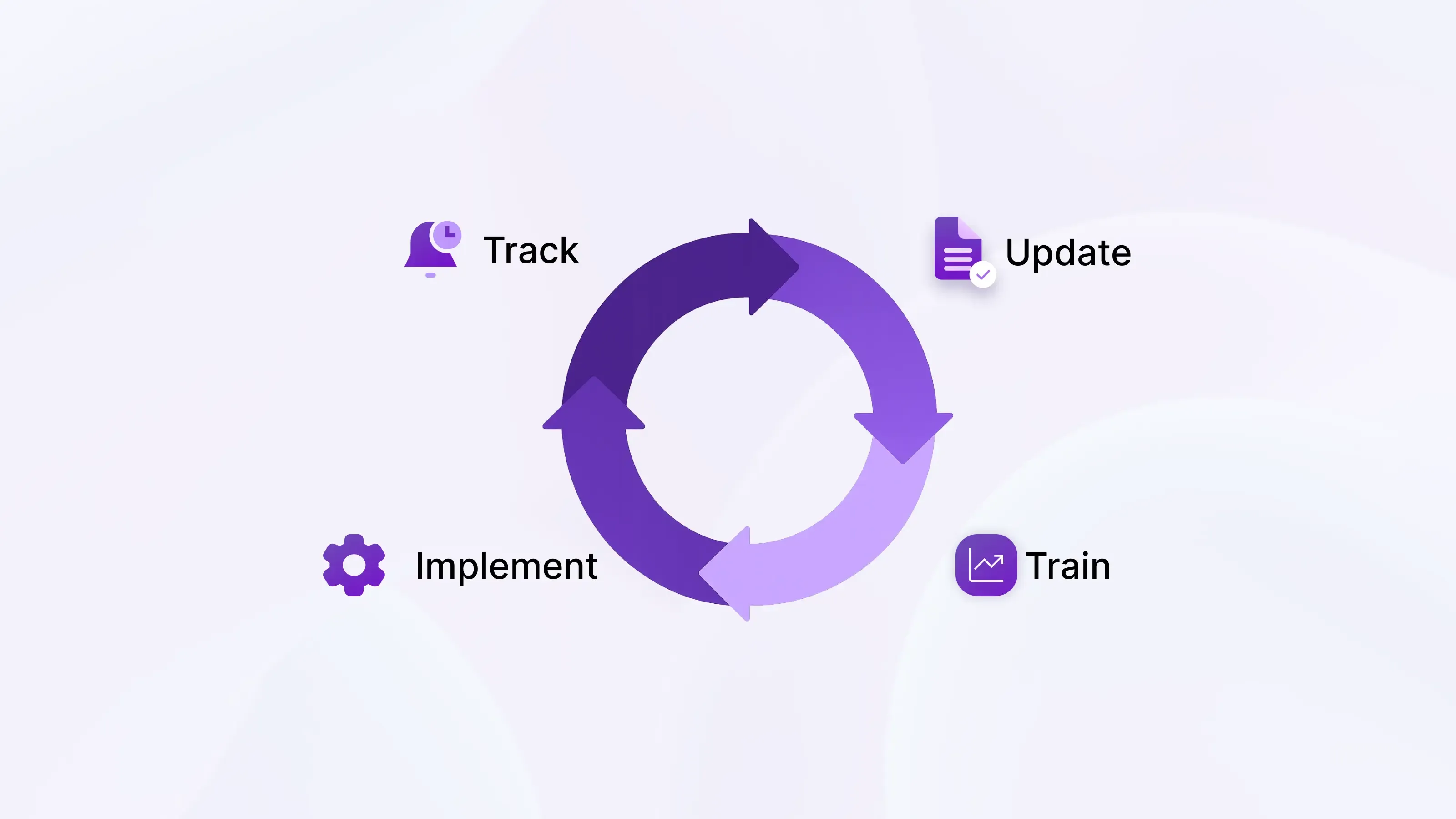

Step 6: Monitor Changes and Train Your Team

In the ever-changing world of tax compliance, tax laws, regulations, and reporting requirements are constantly evolving, and a failure to keep up can expose your business to significant risks.

The final and ongoing step in any robust tax compliance program is to actively monitor changes and ensure your team is properly trained to adapt.

- Subscribe to official gazettes and industry newsletters.

- Hold monthly knowledge sessions summarizing rule changes.

- Update your process maps within 48 hours of a new obligation.

Staying Ahead Internationally

For a global perspective on changes in e-invoicing, real-time reporting, and compliance requirements, check out Global Trend – Electronic Invoicing and Digital Tax Reporting.

Quick Checklist Recap

Before wrapping up, let's take a moment to recap the essential steps for building a resilient tax compliance program.

This isn't just a list of tasks; it's a strategic framework for protecting your business from the costly risks of non-compliance. By following these steps, you’ll transform a reactive, stressful process into a proactive, systematic approach

- Map all tax rules affecting each entity

- Document a repeatable framework with clear owners

- Clean and validate source data

- Store airtight documentation for audits

- Meet every filing deadline

- Monitor legislation and train staff continuously

Conclusion

Regulatory tax compliance protects businesses from financial loss and reputational harm. By building a strong framework and staying audit-ready, finance leaders can navigate complex obligations with confidence. A proactive tax and compliance approach secures long-term stability and trust.