Margin Variance Check

If your EBIT margins diverge substantially from comparable benchmarks, it may trigger tax authority scrutiny. It’s prudent to compile a defense file or consider pricing adjustments before year-end to mitigate risk.

Step 5: Automate Data Collection and Reconciliation

Manual spreadsheets struggle with multi-country complexity. To strengthen your cross-border tax & accounting framework:

- Integrate your systems: Link ERP, e-commerce platforms, and bank feeds with a tax engine to centralize data and reduce errors.

- Schedule frequent reconciliations, ideally nightly, so anomalies emerge while transactions are still fresh.

- Maintain complete digital audit trails - line-level data is required for compliance with EU SAF-T and France’s FEC standards.

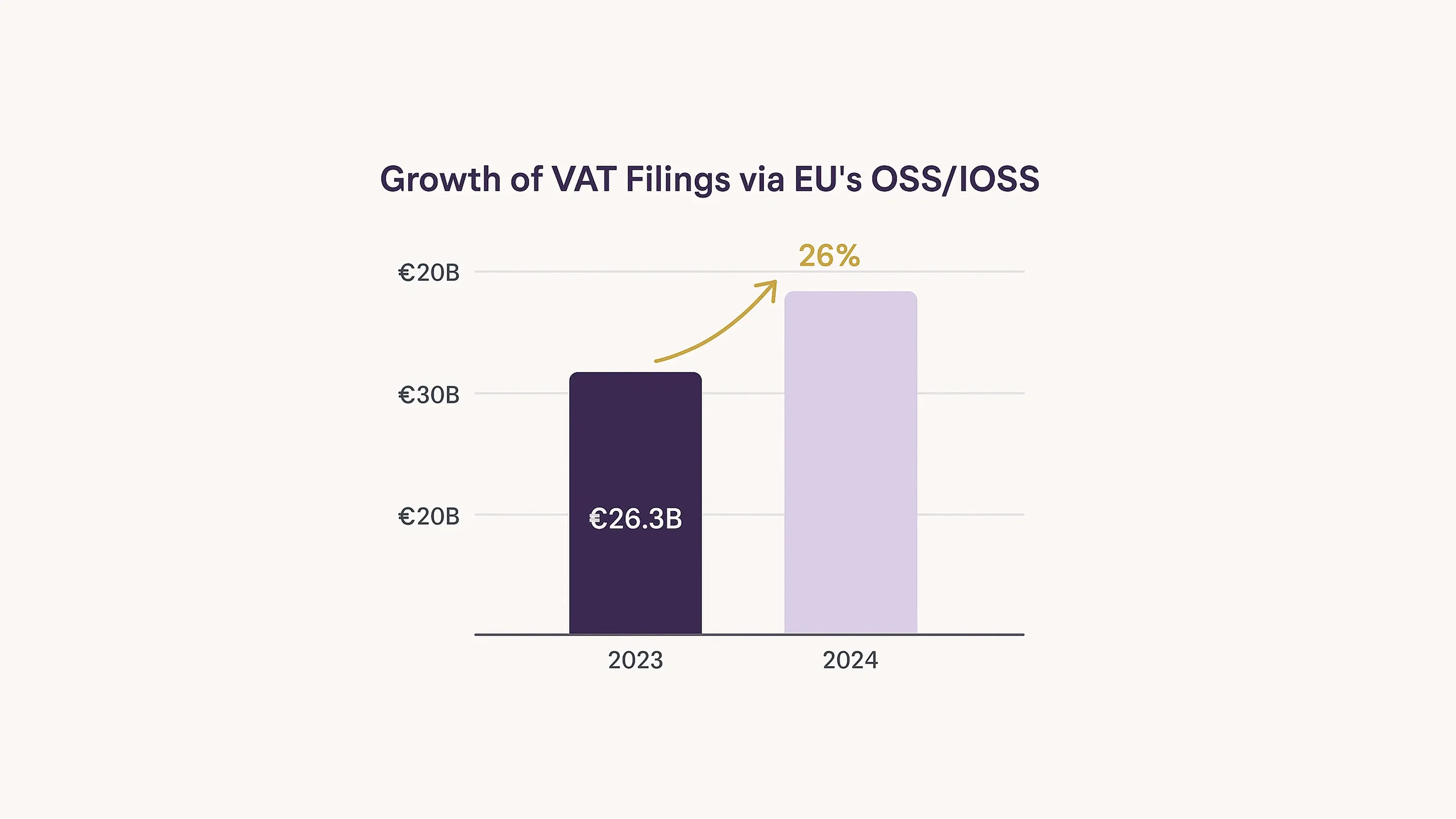

For more on automating VAT compliance, consult industry-respected resources like Tax Technology Tools – VAT Compliance Automation.

Choosing tools

When evaluating cross-border tax solutions, prioritize platforms that support multi-currency and multi-language ledgers, automatically maintain tax rate libraries, and integrate with your existing systems. Opting for a subscription-based solution is often more cost-effective and scalable than building and maintaining custom tax tables in-house.

Step 6: Leverage Cross-border Tax Solutions and Experts

Even the most advanced tax technology should be complemented by professional expertise. OECD guidance stresses the importance of qualified tax professionals in ensuring compliance across jurisdictions.

- Engage reputable global or local tax advisory firms - professional advisers can handle complex cross-border tasks, such as acting as an IOSS intermediary or managing Canadian NRI registrations, where in-depth local knowledge is essential.

- Consider fixed-fee agreements - while not mandated, fixed-fee packages can improve budget predictability and are a common practice among multinational SMEs.

- Review service agreements regularly - OECD highlights that periodic evaluation of service provider performance helps ensure value and compliance, though it does not set a specific review frequency. Many businesses choose quarterly or semi-annual reviews to align with transaction volume changes.

Step 7: Monitor Regulatory Change and Information Exchange

According to the OECD’s Automatic Exchange of Information 2024 report, 134 million financial accounts are now automatically exchanged across 111 jurisdictions (OECD AEOI). This unprecedented transparency means tax authorities can quickly identify inconsistencies in cross-border reporting.

How to stay compliant:

- Subscribe to tax authority updates in your key markets.

- Record all auditor requests - they often signal upcoming rule changes.

- Conduct bi-annual compliance checks, testing sample transactions against current rules.

- Track e-invoicing and digital reporting requirements to avoid last-minute compliance gaps.

Stay ahead of worldwide compliance changes and digital reporting obligations in Global Trend – Electronic Invoicing and Digital Tax Reporting.

Prepare for pillar-two and e-invoicing

Pillar Two’s 15% minimum tax and expanding e-invoicing in countries like Italy, France, and Poland will raise data demands - update your ledgers now to stay compliant.

Conclusion

Cross-border tax & accounting isn’t a guessing game. Map your flows, secure indirect taxes, align reporting calendars, document transfer pricing, automate data work, work with the right experts, and stay ahead of regulatory changes. Follow these seven steps, and you’ll spend less time racing deadlines - and more time driving your SME toward confident, profitable international growth.