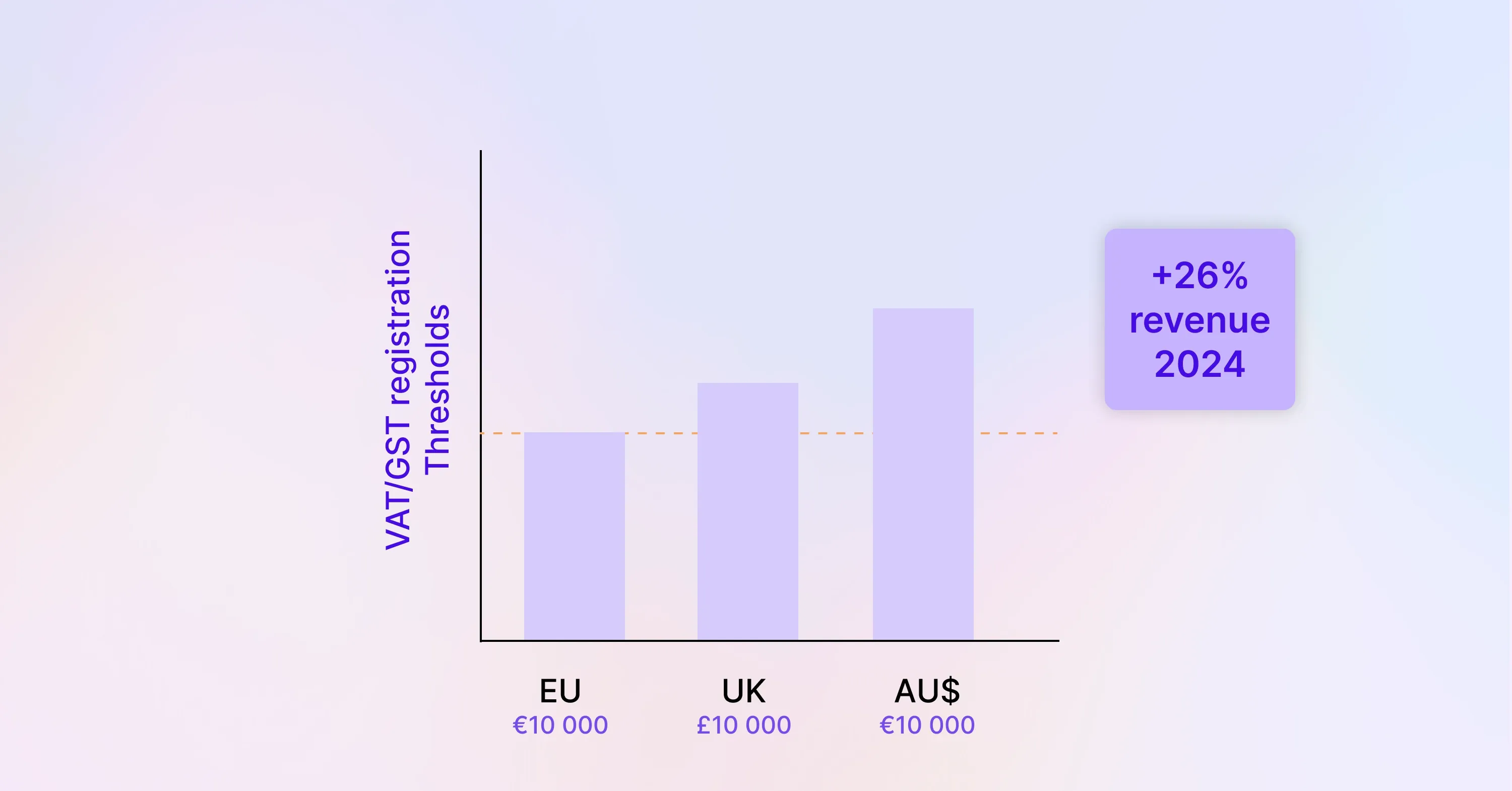

Apply for VAT/GST numbers

- Submit the VAT1 (UK) or Form RC1 (Ireland) online.

- Select standard, flat-rate, or OSS/IOSS schemes if selling across borders.

- Provide evidence of cross-border sales or intent to trade.

Outsource wisely: Firms like 1stopVAT, whose 40+ specialists cover 100+ countries, can act as a single contact point for international VAT filings, sparing you multiple portals and languages.

Transition: Once your VAT or GST number arrives, display it on invoices and update marketplace dashboards to prevent account suspension.

Step 5: Set Up Payroll and Withholding Taxes

Hiring even one employee triggers new duties.

Key actions

- Register for Pay-As-You-Earn (PAYE) in the UK or Federal/State withholding in the US.

- Obtain unemployment insurance and workers’ compensation numbers.

- Decide on pay frequency and submit Real-Time Information (RTI) or equivalent.

Example: A small café in London that misses its first RTI submission faces an immediate £100 penalty and daily surcharges if the lapse continues.

Takeaway: Accurate payroll registration protects staff morale and avoids spiraling fines.

Step 6: Understand Local and Industry-Specific Levies

Besides national taxes, you may face:

- Business rates or property tax.

- Digital services tax.

- Environmental levies (plastic packaging, carbon credits).

- Tourism or city taxes for hospitality trades.

Tip: Search municipal websites or call the local chamber of commerce early to identify hidden obligations.

Step 7: Build an Ongoing Compliance Calendar

A registration certificate is just the start.

- Record filing deadlines: corporation tax, VAT returns, payroll filings, statutory accounts.

- Map payment due dates and set bank reminders.

- Assign responsibilities between founders, accountants, or external advisers.

For best practices on designing a tax calendar and aligning global reporting periods, see Aligning Cross-Border Tax and Accounting Practices for SMEs.

Why it matters: Compliant companies in the UK still spend at least £15.4 billion a year meeting tax duties, and a further £46.8 billion in unpaid tax forms the UK’s “tax gap.” A clear calendar keeps you out of both groups.

Business tax registration

Business tax registration is the process of officially notifying tax authorities that your new venture exists, obtaining ID numbers for corporate income tax, VAT or GST, payroll, and any local levies, then keeping those accounts active through regular filings and payments.

Conclusion

Registering your venture for taxes is less about ticking boxes and more about building a reliable platform for growth. By confirming your legal structure, gathering the right documents, and sequentially registering for corporation tax, VAT, payroll, and local levies, you sidestep penalties and preserve cash for expansion. Treat tax registration as an investment in credibility and peace of mind, and your business will be ready for whatever opportunities come next.

For more actionable breakdowns and checklists, see the VAT Compliance Checklist for Startups and Small Businesses