In our Beginner’s Guide to VAT Compliance, we are showing you how to navigate through the maze of VAT terminology and related processes with as much ease as possible.

What is VAT?

Value-Added Tax or VAT is a consumption tax placed on almost all supplies of goods and provision of services. However, some supplies are VAT-free or to be precise tax-exempt. The tax revenue based on the OECD reports contributes to the country’s GDP, which is, on average, between 17% and 47% (VAT Notice 700). Gathered VAT plays a significant role in this.

Yearly reports conducted by the OECD concerning the tax contribution to the country’s overall GDP indicate that VAT is a major contributor to the country’s tax revenue. In developed countries, on average VAT contributes to 25% of the overall tax revenue. In developing countries, that level goes even higher and reaches up to 35% of the country’s overall revenue (VATabout).

VAT is levied on each stage of the supply chain, covering all steps in the distribution or production.

Considering the relevance of VAT to the country’s revenue, being familiar with the tax itself, its structure, rules, and regulations is of great importance for the economic operator. The future of business prosperity is closely connected to how the VAT compliance is handled.

Key Principles for Understanding VAT and VAT compliance

One of the questions that we often encounter from a part of our clients that are just starting in the business world, can be summarized as What is VAT compliance? VAT compliance concisely covers a broad range of requirements and responsibilities that a taxable person has towards the VAT rules established at the level of the country or an international level, depending on, e.g., the place of business activity or place of taxation (VAT Notice 700).

I know, this still sounds to a large extent very enigmatic, and you would surely prefer that we take a few steps further to demystify the Global VAT compliance rules so you can understand what this fuss is all about, and what will be the possible ways to approach your potential or actual tax duties.

We should move further with our understanding of the VAT concept, by making a VAT compliance checklist, where we would together tackle the most essential elements of VAT compliance. We would approach this endeavor through lenses of possible stakeholders, such as retailers, e-commerce suppliers, or digital service providers.

Free VAT Compliance Guide

Ensure your business stays VAT-compliant with our essential guide. Learn how to navigate VAT regulations, avoid costly mistakes, and streamline tax processes.

✅ Understand VAT fundamentals

✅ Simplify registration and compliance

✅ Avoid common VAT pitfalls

✅ Stay updated on regulations

The main terms, and accompanying definitions, are primarily similar when it comes to rules and requirements, no matter the type of VATable person. Still, there is also a considerable difference regarding the reporting rules for businesses that operate cross-border, and make their supplies using digital channels instead of making their supplies in a “traditional” brick and mortar way.

So, take your seats, make a good espresso, and let’s move further with our walk through the VAT terminology, rules and regulations.

Registration thresholds

Who needs to register for VAT?

One general question that many business owners or businesses ask is whether all businesses need to register for VAT and charge VAT. The simple answer is no, definitely not. Only VAT-registered businesses should charge VAT on their supplies.

In many countries, there is a so-called small business scheme. If the country has this beneficial regime in place, it permits economic persons to make their supplies or provision of services without the necessity to register for VAT and to charge it (VAT Notice 700).

However, the beneficial scheme for small businesses comes with a turnover condition. When the vendor reaches a sales turnover of X amount, it is obligated to register for VAT and charge it. Most countries have no registration threshold when businesses exclusively make tax-exempt supplies.

When the vendor reaches the registration threshold, he is obligated to register for VAT on time and according to the stipulated requirements. Businesses that register for VAT late will often pay the penalty for being late with their registration, and on top of that, they will need to pay fines and interest for all the VAT payable that they should have collected from their clients from the moment they should have been registered.

The VAT registration requirements vary from country to country. The registration thresholds are different between countries and within a country depending on the type of business activity. The scope of documentation that needs to be submitted also varies depending on the applicant’s place of business.

Many more conditions need to be considered for a business that must be registered.

What obligations do VAT-registered businesses have?

After successful registration, the minimum scope of VAT obligations for businesses is the following:

- Charge and collect VAT at the proper tax rates and conditions on all taxable supplies

- Issuance of compliant VAT accounting documents(tax invoices, credit and debit notes, sales receipts) (VAT Notice 700/21).

- Submission of VAT returns following the fixed reporting period and deadline

- VAT payments by due date (VATabout).

- Keeping of proper VAT records and respecting the retention period of documentation in scope (VAT Notice 700/21).

Why should taxable persons register at the right time?

We recommend that business owners familiarize themselves with the VAT framework in their place of business or establishment before starting their business or registering it. A basic understanding of the VAT requirements could prevent many difficulties from arising when the business does not follow the mandated requirements (VAT Notice 700)).

The existence of the small business scheme permits most domestic businesses some sort of “free pass” for making taxable supplies within the boundaries of their country. However, the exact scope of small business schemes cannot be counted for if the business makes cross-border supplies or exclusively some B2C supplies.

When it comes to the rules for VAT registration for e-commerce businesses or digital service providers, the situation for understanding the applicability of rules becomes even more complicated, because now the business owner needs to expand his sales tax understanding also in connection with the regulations of the countries where it makes its sales.

Being VAT registered within mandated timeframe is of high importance. Late VAT registration often bears the payment of the penalty for late registration, which potentially will be aggregated with the penalty for late submission of VAT returns, and the connected interest on all of that.

Late registration could potentially make claiming input tax credits impossible, damage the business’s reputation, and limit the scope of partnerships with VAT-registered businesses.

What VAT rate do I have to charge?

The VAT rate that should be charged depends on the type of supply made. The VAT rate is conditioned by the type of good or service sold. In some cases, the VAT rate of one item depends on the VAT rate of other items/goods/services that are part of the transaction.

Significant differences exist in tax rates and categories of tax rates countries have adopted (VAT Notice 700)). Many VAT countries have a general or standard VAT rate, a reduced and zero-rated supply, and always VAT-exempt transactions.

In what way should I calculate reportable VAT to the Tax Authority?

The VAT that should be paid or reclaimed from the tax authority depends on the value of the output tax(charged VAT), and the input tax(input tax credits). In cases where a taxable person has collected more sales tax than it has paid for the business purchases, the sum of this difference should be remitted to the revenue authority. In cases where input tax credit is above output tax, the tax authority is obligated to reimburse the taxable person.

What are additional requirements for e-commerce sellers?

Technological advancements and digitalization have entirely reshaped the retail business landscape. At present, and without doubt in the future, the e-commerce and digital economy are of essential importance to the business environment.

The benefits of the e-commerce business model made the cross-border transactions and internationalization of trade never easier for interested suppliers and customers. However, with these benefits, new tax and legal requirements have arisen.

The VAT compliance for e-commerce vendors is more complicated in comparison with tax rules and regulations established for traditional business models (1stopVAT), e.g., retail businesses making direct B2C supplies in brick-and-mortar stores.

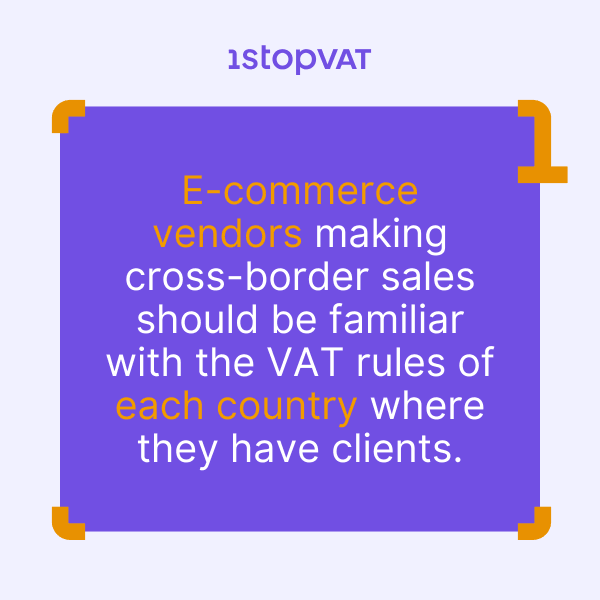

E-commerce vendors making cross-border sales should be familiar with the VAT rules of each country where they have clients. Their VAT compliance includes familiarizing themselves with registration thresholds and reporting, recording, and retention requirements at the level of each country where their clients are located.

What are additional requirements for digital service providers?

Suppliers of digital goods or digital services, such as direct vendors that make their sales through their website or other type of digital channel or digital platform operators, are similarly also e-commerce vendors obligated to get familiar with the VAT rules at the level of each country or territory where they make their supplies (1stopVAT).

What records do I need to keep for VAT?

One of the primary elements of the VAT compliance for VAT-registered businesses is to follow proper record-keeping requirements.

Maintaining business records with accompanying documentation is important for establishing a compliant VAT framework. The business records should generally be complete and up-to-date and support the claims and calculations made in the tax returns (VAT Notice 700/21).

The scope of business records varies from jurisdiction to jurisdiction, but mainly it covers the proper maintenance of the following documentation:

- purchase and sales books;

- annual accounts;

- credit and debit notes;

- order and delivery notes;

- import and export documents;

- purchase and sales invoices;

- VAT account.

The exact structure and content of the business records depend on the type of business activity that a VAT registered taxable person practices.

Tax Penalties

How to avoid tax penalties?

After the VAT registration, the taxable person is required to adhere to the rules and regulations of the indirect tax framework. The infringement of these rules will in most cases result in penalties and interest. One of the crucial points of being VAT compliant is the submission of VAT declarations and VAT payments on the due dates (VATabout).

When the taxable person files a return late or makes VAT payment late, in most cases, they will incur additional burden translated into the payment of a penalty to the tax authority and interest for the owed VAT. To take one step back, it’s of fundamental importance that the tax calculations on the previously issued invoices/receipts have been done correctly. The best practice for that is having a proper tax calculation software, with the integrated functionality of all VAT rates that are continuously monitored and updated when necessary.

Wrongful calculations lead to incorrect invoices and returns. This will probably result in penalties for the vendor and the impossibility for the buyer(if it’s a B2B supply) to record the purchase transaction correctly and claim input tax credits.

Backdated VAT registration

Taxable persons who haven’t registered for VAT by the due date could face a penalty for late registration. In addition to the principal penalty, they could face penalties and interest for non-submission and payment of VAT due for the look-back period.

Certain taxable persons can apply for a backdated VAT registration in many jurisdictions. This has pros and cons. One benefit is the possibility of claiming input tax credits for the applicant’s business purchases in the look-back period. In some countries, the respective tax authorities have prepared an explanatory backdated VAT registration guide.

Other benefits include reduced penalties, interest, and possible costly tax audits, which will occur if the state revenue authority notices an infringement of a non-registered taxable person.

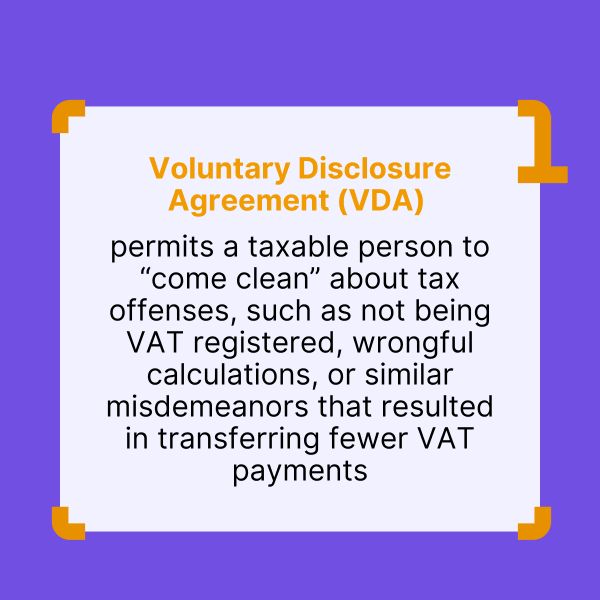

Voluntary Disclosure Agreement(VDA)

In many jurisdictions, the economic operators have the possibility to “limit their tax liability” by signing a Voluntary Disclosure Agreement with the revenue authority. VDA permits a taxable person to “come clean” about tax offenses, such as not being VAT registered, wrongful calculations, or similar misdemeanors that resulted in transferring fewer VAT payments (1stopVAT).

Not all jurisdictions have provisions permitting businesses to enter into VDAs. The application for the VDA, negotiations with tax officials, and signing of the VDA are very demanding procedures that require a skillful tax advisor.

The successful negotiation that resulted in the signing of the agreement permits a taxable person to limit its tax exposure to a much lesser period compared to the results guaranteed as the result of the tax audit.

The VDA will reduce interest or remove it entirely from the tax liability calculation, reduce penalties, cut the look-back period, and could also permit businesses to claim input tax credits. The business’s credibility will be significantly higher than it would be if the clients become familiar with the vendor’s non-compliant behavior.

Role of the Third Party Service Providers

In many cases the cross-border e-commerce vendors and digital service providers acquire services of third-party VAT service providers. One should bear in mind that the tax provisions that coordinate the cross-border transactions in this ecosystem are new, changing rapidly, defragmented, open to interpretation, and there are much more challenges in comparison to traditional retail operations .

In the last ten years, the number of VAT consulting and advisory-related service providers has increased exponentially, which seems logical. It is directly proportional to several e-commerce vendors and digital services providers that are or should be treated as VATable persons.

Some of the key areas where taxable persons acquire services of the service providers are:

- Registrations – overview of global tax exposure and consultation on registration requirements in all jurisdictions where it’s needed;

- Tax Calculations – digital calculations(automatized or semi-automatic) depending on the type of software solution used;

- VAT-rate updates – well-maintained database of all related VAT rates, and continuous automated updates and notifications when a change happens;

- Reporting – submission of VAT returns and remittance of tax (manual, digital or automatic);

- VAT monitoring – monitoring of the tax landscape of interest and prompt notification.

One of the biggest challenges on how to stay VAT compliant in this rapidly changing tax landscape is one of the first questions that the business owners should ask themselves if they want to establish a profitable business for X number of years. The credibility, reputation, and good business practices are more important than ever in this space, due to vast competition, and easily reachable information about misdeeds.

Free VAT Compliance Guide

Ensure your business stays VAT-compliant with our essential guide. Learn how to navigate VAT regulations, avoid costly mistakes, and streamline tax processes.

✅ Understand VAT fundamentals

✅ Simplify registration and compliance

✅ Avoid common VAT pitfalls

✅ Stay updated on regulations