One of the primary goals behind reshaping the EU SME’s legal framework was to introduce a mechanism that would equalize the playing field between domestic and non-domestic EU-established small enterprises regarding their VAT compliance obligations in the Member States(MS) where VAT is due.

The current tax landscape for SMEs is entirely based on the concept of domestic SME schemes. From a VAT perspective, only small enterprises established in the Member State where VAT is due could adhere to the SME scheme. Naturally, the possibility of leveraging from the domestic VAT scheme is reserved only for local small enterprises that fulfill national requirements.

The shift from the place of supply rules, from the origin to destination principle, created significant administrative and compliance difficulties for small enterprises not established in the Member State where VAT is due. This means that they need to follow the tax rules of the MS where VAT is due.

The introduction of the cross-border SME scheme concept from January 1, 2025, will significantly change the rules surrounding the small enterprises established in the EU that make their supplies of goods and services in other Member States.

The cross-border SME scheme concept will permit small enterprises established in one Member State to remain VAT-exempt in one or more MS where they have customers(and in which occasions the VAT is due) if specific mandatory requirements are met.

Principal requisites that SMEs should meet if they plan to make intra-EU supplies that are VAT-exempt could be summarized in a few points:

- To register for a cross-border SME scheme.

- To maintain the annual EU-based turnover below EUR 100 000.

- To not surpass the annual nationally based Member State threshold for small enterprises.

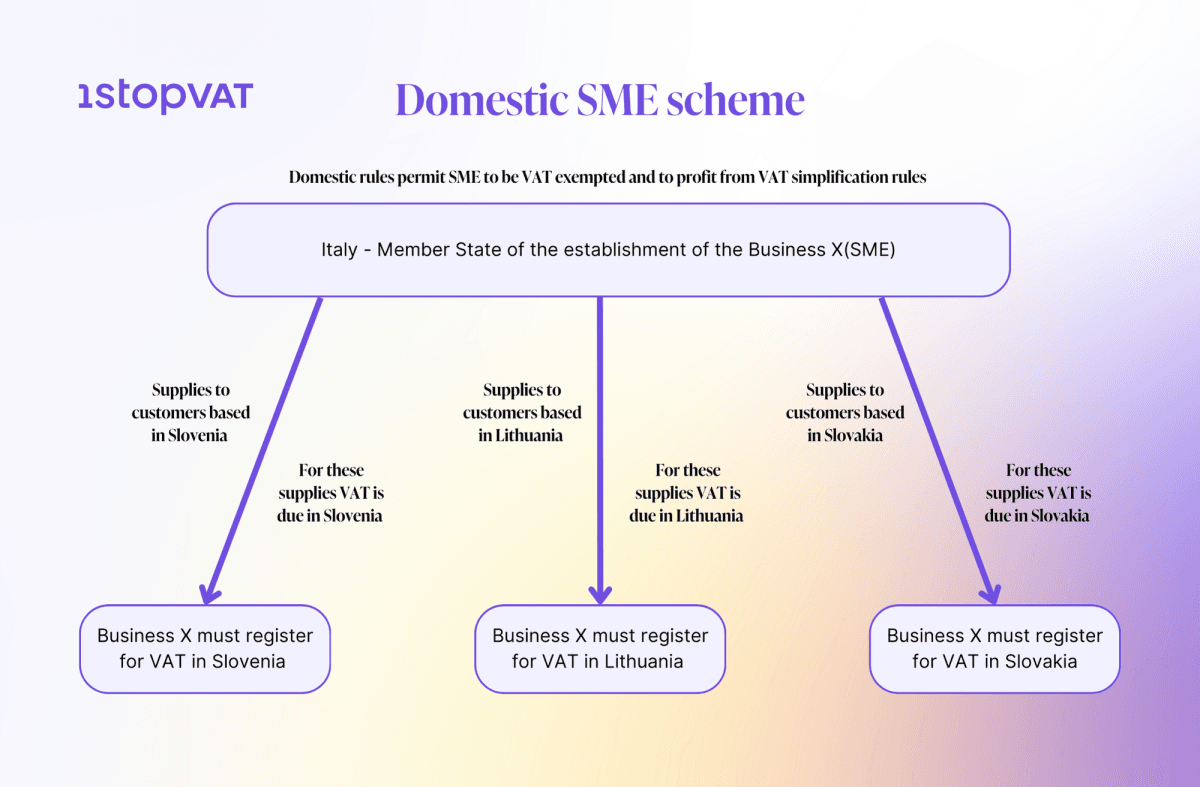

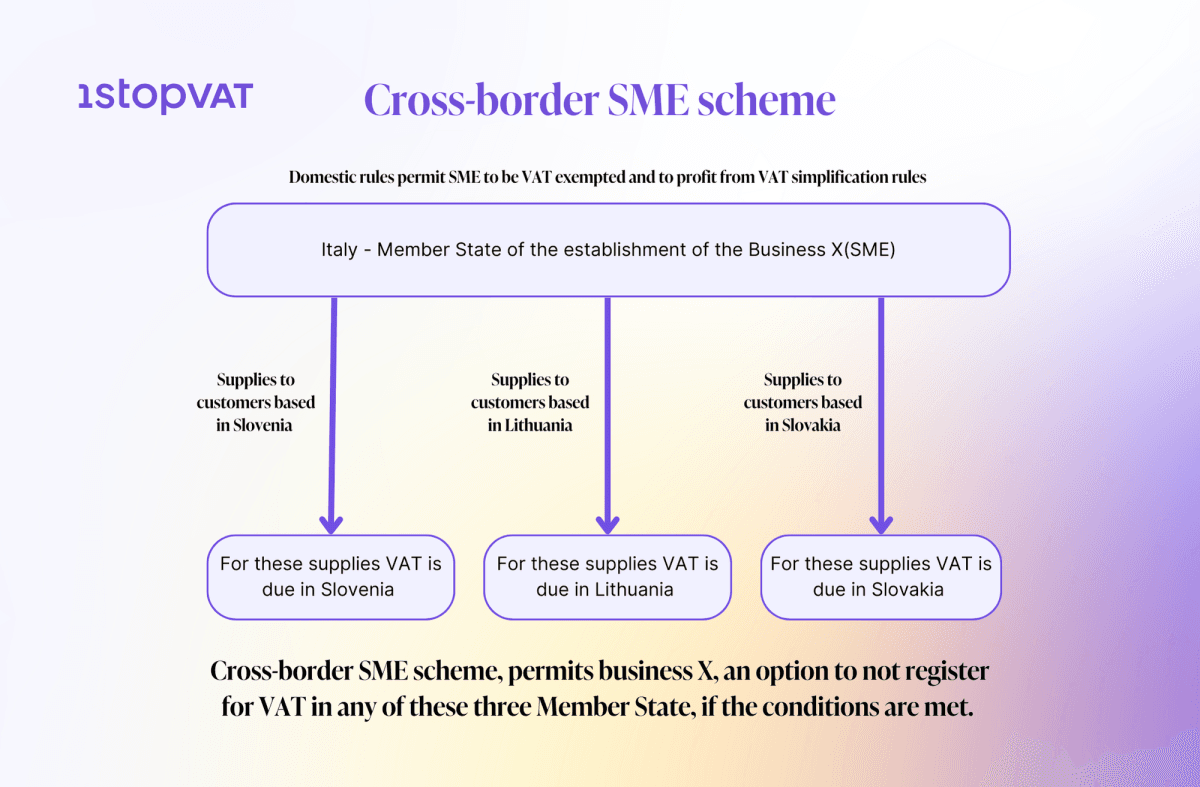

Take a look at the schemes provided below to better understand the new rules governing the domestic SME scheme and the cross-border SME scheme(cross-border VAT exemption scheme).

If you want to learn more about domestic and cross-border SME schemes, please review our previous article.

The first scheme shows the current rules and scope of the SME scheme. A small enterprise can leverage the domestic SME scheme only for supplies made within its country of establishment. If it makes supplies in other Member States in which VAT is due, it must register following the standard VAT registration procedure.

The second scheme shows in a general manner what benefits concerning VAT simplification will be introduced through the introduction of the cross-border SME scheme. This simplification scheme will permit a small enterprise established in the EU to profit from the possibility of remaining exempted from VAT duties in other Member States in which VAT is due. Of course, this will be possible only if the specific conditions are met.

The EU institutions have adopted a series of legislative measures to reduce the compliance costs of EU-based small enterprises. Introducing the cross-border SME scheme will unquestionably decrease the number of mandatory VAT registrations and related compliance costs that small businesses encounter for their taxable supplies.

However, to profit from this tax relief, small enterprises that supply goods or digital services, such as intra-community distance sales, should pay close attention to whether they meet the newly established requirements.

Aleksandar Delic

1stopVAT Senior Indirect Tax Researcher (Global Content)

Register for a FREE consultation

We offer a FREE consultation to better understand your needs. This could result in a simple solution to your taxes issues or lead to a more collaborative working relationship. Let’s find out what’s the best solution for you!

Book a Free consultation